A bad quarter becomes a bad year faster than most investors expect. The account statement drops. The explanation from the broker feels polished but thin. You start asking basic questions that should have been easy to answer from the beginning. Was this investment even suitable for me? Did anyone else complain about this advisor? Was there a history I never saw?

Those questions often lead to one of the most useful records in securities law, the central registration depository. For investors, the CRD is not just a database regulators use behind the scenes. It is often the first place where a pattern starts to show. A job termination that did not make sense at the time. A disciplinary event. A customer dispute that sounds a lot like your own experience.

If you would like a free consultation to discuss the investment loss recovery process in more detail, call Kons Law Firm at (860) 920-5181 for a FREE, NO OBLIGATION consultation.

Good investing starts with prevention, and broad education helps. A practical primer on top financial risk management strategies for investments can help investors think more carefully about concentration, suitability, and downside exposure before losses pile up. But once money is already gone, the issue becomes evidence. You need records, timelines, and facts that can support a claim.

The CRD matters because it can do both jobs. It helps investors vet a broker before investing, and it helps build a case after misconduct has already happened. That is why understanding the regulatory system also matters. If you are not clear on the regulator’s role, this overview of what FINRA does provides useful context for how broker oversight, registration, and dispute resolution fit together.

Your Investment's First Line of Defense

An investor usually does not come looking for the CRD on a good day. They come after an account falls sharply, after they discover trades they did not approve, or after they learn a supposedly conservative recommendation was loaded with risk.

In that moment, investors often focus on the product. The annuity. The private placement. The non-traded REIT. The options strategy. The better question is often about the person who sold it.

Where the first answers usually appear

The central registration depository is often where the paper trail starts to become visible. A broker’s history may show prior complaints, licensing issues, employment changes, or disciplinary disclosures that should have raised concern earlier. For an investor trying to understand whether losses were the result of market risk or misconduct, that distinction matters.

A clean sales presentation can hide a problematic record. The CRD helps cut through that. It can reveal whether the recommendation came from a professional with a stable background or from someone with a history worth closer scrutiny.

Practical takeaway: If you suspect broker misconduct, do not rely on memory or verbal explanations. Start preserving records and checking the advisor’s background immediately.

Why this matters after losses occur

Investors often assume background checks are only useful before they hire someone. In practice, CRD information can be just as important after the damage is done. It helps answer questions like these:

- Was there a pattern: Has this broker faced similar complaints from other customers?

- Was supervision weak: Did the firm keep employing the broker after prior disclosure events?

- Was the risk obvious: Did the broker have a history that should have triggered tighter oversight?

Those questions do not resolve a case by themselves. But they can shape the theory of liability early. In many disputes, that is the difference between a vague grievance and a focused claim supported by records.

Unpacking the CRD System

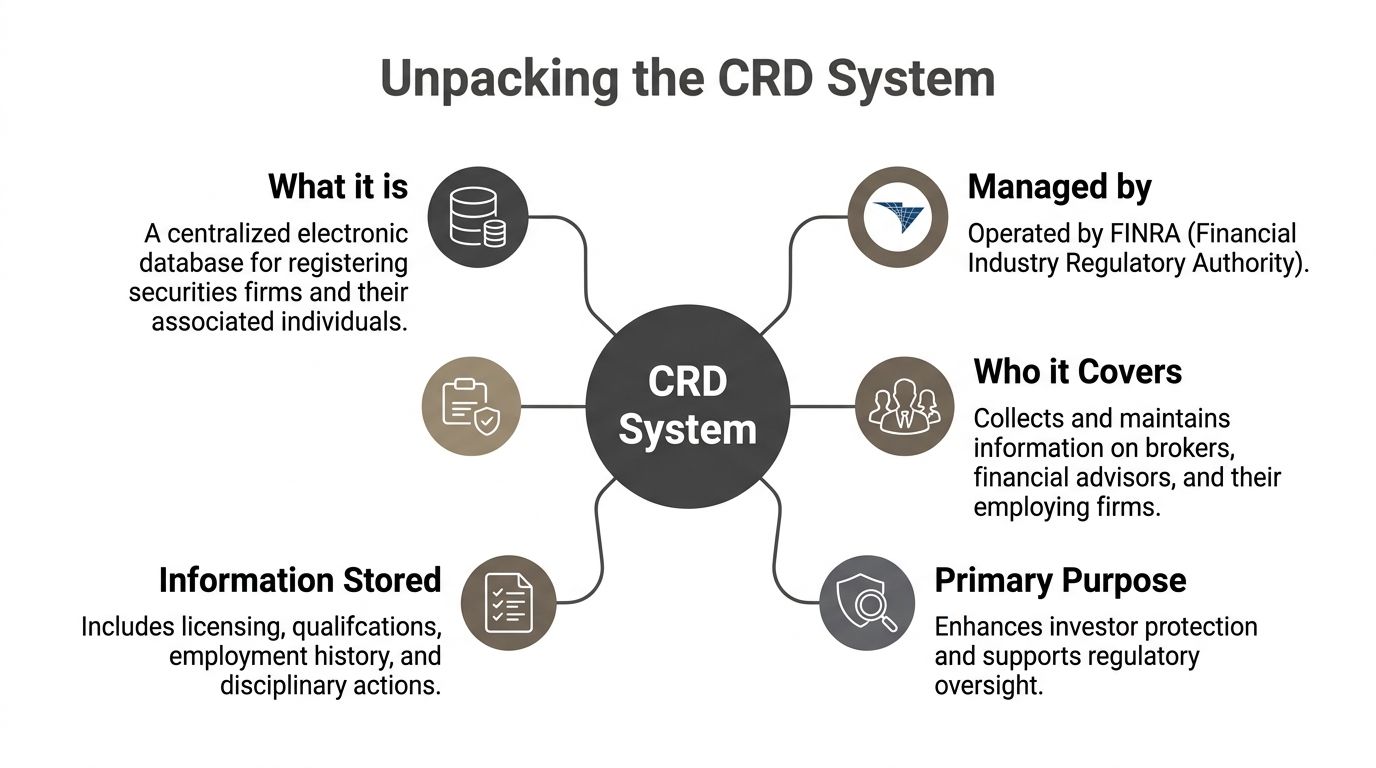

The easiest way to think about the central registration depository is this. It is the securities industry’s permanent record system for brokers and brokerage firms.

It is not a marketing profile. It is not a résumé written by the advisor. It is a centralized regulatory database built to track registration, licensing, employment history, and disciplinary information across jurisdictions.

What the system is

The Central Registration Depository, developed by NASAA and NASD and implemented in 1981, consolidated fragmented state paper processes into one nationwide computerized database. Today it maintains licensing and disciplinary histories on more than 630,000 securities professionals and nearly 4,000 broker-dealer firms, and it serves as the backbone for BrokerCheck, according to NASAA’s CRD and IARD overview.

That history matters because it explains why the CRD remains so useful in modern disputes. Brokerage activity is not confined to one state, one office, or one branch manager. Misconduct can follow a broker from firm to firm unless there is a system that preserves the record.

Who uses it and why

Regulators use the CRD to monitor registration and disclosures. Brokerage firms use it for filings, updates, and employment-related records. Investors encounter part of that information through BrokerCheck.

The public never sees everything that exists in the underlying regulatory ecosystem. But the data that does surface often tells you more than an advisor’s website ever will.

A few practical examples:

- Registration history: Whether the person was properly licensed when recommendations were made.

- Employment movement: Whether the broker moved frequently between firms.

- Disclosure events: Whether there were customer disputes, regulatory actions, or other reportable matters.

For firms and compliance teams, CRD data is operational. For investors, it is risk screening. For attorneys, it becomes evidence.

What works and what does not

What works is using the CRD as a starting point for verification. It is especially useful when an investor was told, implicitly or directly, that the advisor had an unblemished history.

What does not work is treating the system like a complete biography. It is a regulatory record, not a full narrative. You still have to read it carefully, compare it to account documents, and test what the broker told you against what was filed.

For readers who want broader operational context on the compliance side, Mastering Compliance in Financial Services Industry is a useful companion piece because it helps explain why registration systems and reporting duties matter in day-to-day brokerage supervision.

Key point: The central registration depository is most powerful when you use it as a verification tool, not as a substitute for deeper investigation.

Using BrokerCheck to Vet Your Financial Advisor

Investors do not access the CRD directly. They use FINRA BrokerCheck, which is the public-facing tool built from CRD data.

According to Finance Strategists’ overview of the Central Registration Depository, BrokerCheck provides public access to CRD data on over 660,000 active individuals and more than 6,800 registered firms. It processes registration, update, and termination filings so investors can review licensure and disclosure information before problems become bigger losses.

How to run the search

Start with the individual broker’s full name if you have it. If the name is common, add the firm name or location. If you only know the firm, search the firm first and work backward to the advisor.

When you open a report, focus on the basics before you get lost in detail.

Confirm identity

Make sure you have the right person. Similar names are common.

Check current and prior firms

Employment history can reveal frequent moves or short stays.

Review licenses and exams

This helps answer whether the person was registered to do what they were doing.

Look for disclosures

These are the sections that often matter most in an investor dispute.

What you should pull from the report

A BrokerCheck report can help you answer practical, not academic, questions:

- Did this person sell products in states where they were licensed

- Were there prior complaints before my losses happened

- Did the broker change firms shortly after customer issues arose

- Was there a termination or disclosure that needs more explanation

If your concern involves an employment exit, this background on the U-5 form and FINRA helps explain why termination-related filings can matter so much in later disputes.

What to save right away

Do not just read the report and move on. Download it and keep a copy. Reports can change as filings are updated, amended, or supplemented.

Save these items in one folder:

- The full BrokerCheck report

- Recent account statements

- Emails or text messages with the advisor

- Notes of meetings or calls

- Product paperwork and risk disclosures

That basic file often becomes the foundation for a stronger legal review later.

Tip: Save the report the day you find it. In a dispute, timing matters, and a preserved copy is often more useful than a later recollection of what you think it said.

Decoding Disclosures and Disciplinary History

A disclosure is not an automatic finding of wrongdoing. It is a signal. Some signals are weak. Some are serious. The skill is learning which ones deserve immediate attention.

CRD reporting requires disclosure across 19 event categories on Form U4, including arbitrations over $15,000 and customer complaints alleging theft or forgery. The same source states that brokers with 5 or more disclosures have a three times higher rate of FINRA enforcement actions, which is why patterns matter so much when investors review a record, as explained in InnReg’s discussion of FINRA CRD disclosures.

The disclosure types that deserve close review

Not every disclosure carries the same weight. A practical reading looks for relevance, repetition, and factual similarity to your own experience.

Customer disputes often matter most to harmed investors. If prior customers alleged unsuitability, unauthorized trading, misrepresentation, excessive trading, or concentration in risky products, that can be highly relevant.

Regulatory actions can show that a regulator already identified conduct problems. Even when the conduct differs from your case, it may still speak to supervision and credibility.

Employment separations and internal allegations deserve careful attention. A broker leaving one firm under difficult circumstances can be significant, especially if the conduct later resurfaces elsewhere.

Financial events such as liens, judgments, or bankruptcies do not prove misconduct. But they can matter when the allegations involve selling pressure, product pushing, or questionable outside activity.

What experienced reviewers notice first

A single complaint with thin facts may mean little. A pattern of similar complaints means much more.

Look beyond the existence of a disclosure and ask:

- Do multiple customers describe the same conduct

- Did complaints cluster around a specific investment product

- Did the broker move firms after issues started

- Did the firm keep the broker in place despite warning signs

A report should be read like a timeline, not like a checklist.

| Red Flag Category | What to Look For |

|---|---|

| Customer disputes | Repeated allegations involving the same sales practice, product type, or risk mismatch |

| Regulatory matters | Findings or sanctions that suggest supervision, honesty, or sales practice problems |

| Employment history | Frequent firm changes, short tenures, or departures that raise follow-up questions |

| Product concentration | Disclosures tied to one category of complex or illiquid investments |

| Financial pressure indicators | Events that may suggest incentive pressure, though not misconduct by themselves |

Terms that often require caution

Some report language sounds neutral but deserves follow-up. Phrases can understate the seriousness of what happened.

Examples include:

“Denied” or “contested”

That tells you the allegation was disputed, not that it was false.“Settled”

A settlement may resolve the claim without admitting liability.“Permitted to resign” or similar phrasing

This can require deeper inquiry into what the firm knew.

If your matter involves pre-enforcement regulatory scrutiny, understanding what a Wells notice is can help you interpret some parts of a broader enforcement context.

Investor rule: One disclosure may be explainable. A repeated pattern of the same allegation is rarely something to ignore.

What BrokerCheck Reports Will Not Tell You

BrokerCheck is useful. It is not complete.

That matters because investors often feel reassured by a report that appears clean on first review. In practice, a clean public report does not rule out misconduct, weak supervision, or a stronger claim than you realize.

The public view is only part of the record

BrokerCheck is a window into CRD data, not the entire file. Some details available to regulators, firms, or through legal process are not fully visible in the public version.

That creates a common problem in investor cases. The broker points to a report and says there is nothing there. The investor assumes that ends the inquiry. It does not.

A public report may not fully reveal:

- The underlying documents behind a disclosure

- Internal firm communications about supervision or complaints

- How a termination was described internally

- Whether a pattern becomes clearer when records are compared across sources

What can mislead investors

Three issues come up often.

First, settlements can be misunderstood. A resolved matter does not automatically establish liability, but it also should not be dismissed just because the language is cautious.

Second, vague phrasing can hide context. Public summaries are often compressed and may not capture the seriousness of the conduct alleged.

Third, absence of detail is not proof of safety. Investors should be skeptical of the idea that no visible disclosures means no problem existed.

Important caution: BrokerCheck is a screening tool. It is not a final due diligence report, and it is not a substitute for case investigation when losses have already occurred.

Using CRD Data to Build Your Investment Loss Case

When an investor hires counsel, the central registration depository becomes more than a background-check tool. It becomes part of the evidence strategy.

A securities case usually turns on a few core issues. What was recommended. Why it was recommended. Whether it fit the investor’s objectives and risk tolerance. What the broker and firm knew, and when they knew it. CRD-related records help frame those questions.

How the data supports legal theories

In unsuitable recommendation cases, registration and disclosure history can help establish context. If a broker had prior complaints involving the same kind of product or the same sales practice, that may support a pattern argument.

In failure-to-supervise claims, CRD-linked filings can help identify what the firm knew about the broker’s disciplinary or employment history. That does not end the case, but it can sharpen the focus on whether the brokerage firm responded appropriately to warning signs.

In unauthorized trading or churning matters, the registration record can be paired with statements, trade confirmations, notes, and communications to build a chronology that is much harder for the defense to blur.

What works in real case development

The most effective use of CRD information is comparative. One disclosure by itself may be easy for a defense lawyer to minimize. A sequence of similar events over time is much harder to explain away.

Useful patterns include:

- Similar complaints from multiple customers

- Movement between firms after disclosure events

- Product-specific complaints that match your losses

- Regulatory issues that overlap with your allegations

Attorneys also use formal process to go beyond public summaries. That can include discovery requests and targeted demands for supporting records. If you want a practical look at that process, this FINRA discovery guide is a helpful reference point.

What does not work

What does not work is overreading a single disclosure or assuming every adverse event proves your case. Strong claims are built by connecting the CRD record to the actual sales conduct, account activity, and investor profile.

The best use of CRD data is disciplined. It identifies themes, pressure points, and inconsistencies. Then those themes get tested against the documents that govern the relationship and the losses.

Take Action to Protect Your Investments and Recover Losses

If you suspect broker or advisor misconduct, speed matters. Documents disappear, memories fade, and online records can change as filings are updated.

A practical response is better than an emotional one. Start building your file now.

A short checklist that helps

Preserve every account record

Keep statements, confirmations, applications, emails, text messages, and notes from calls or meetings.Write out a timeline

Include what you were told, when recommendations were made, and when losses became apparent.Download the current BrokerCheck report

Save the full report for the broker and the firm.List the products involved

Be specific. Name the annuity, private placement, non-traded REIT, options strategy, or other investment at issue.Get the matter evaluated professionally

A legal review can often identify claims and records an investor would not know to pursue alone.

The central registration depository is one of the most practical tools available to investors. Used early, it can help avoid trouble. Used after losses, it can help reveal whether your case is really about market risk or about misconduct, poor supervision, or a sales practice that never should have happened.

If you want help evaluating broker misconduct, advisor negligence, unsuitable recommendations, unauthorized trading, private placement losses, non-traded REIT claims, annuity disputes, or other investment losses, contact Kons Law. The firm handles securities and investment recovery matters nationwide and offers a free, no-obligation consultation at (860) 920-5181.