You may have realized something is wrong only after months, or even years, of trusting an advisor, brokerage firm, or private investment promoter. The account kept producing statements. Explanations sounded plausible. Losses were blamed on the market. Then a new advisor reviews the file, a distribution request gets denied, or you finally compare what you were told against what you own. The first fear is usually the same: is it too late to do anything about it?

Is It Too Late to Recover Your Investment Losses

If you're asking that question now, you're not alone, and you shouldn't assume the answer is yes. Fraud deadlines are real, but they are also more nuanced than most investors are led to believe. In many cases, the most important date isn't when the investment was sold or when the first loss appeared. It's when the fraud was discovered, or when the law says it should have been discovered.

If your documents include foreign-language records, translated offering materials, or communications that need to be reviewed carefully, investors sometimes benefit from using specialized resources such as Translators USA, LLC so key details aren't missed.

A lot of bad guidance on statute of limitations fraud boils down to one oversimplified idea: "the event happened years ago, so the claim is gone." That's often wrong. Concealed misconduct, misleading account statements, rolling misrepresentations, and delayed discovery can all change the timing analysis. That's especially true in investment cases, where the paper trail may look ordinary until someone knows what to look for.

One reason investors get tripped up is that they search for a single deadline when there often isn't one. Court claims, arbitration claims, and potential criminal investigations don't always operate on the same schedule. State law also matters. So does the relationship between the investor and the advisor, and whether the advisor actively hid what happened.

Practical rule: Never decide your case is time-barred based only on the trade date or the year the investment was purchased.

A useful starting point is to review a broader discussion of securities fraud filing deadlines and limitations issues. But the key point is simple. Delay can hurt a case, but elapsed time alone doesn't end it.

What works is an immediate, disciplined review of the documents, communications, account history, and the moment when warning signs first became visible. What doesn't work is waiting longer because you're embarrassed, uncertain, or hoping the firm will fix it informally. In fraud matters, hesitation often creates a second problem on top of the first.

What Is a Statute of Limitations for Fraud

A statute of limitations is a legal filing deadline. Think of it as the clock on your right to bring a claim. When that clock expires, a court or arbitration forum may refuse to hear the case even if the underlying misconduct was serious.

Why this deadline matters so much

Many investors assume deadlines work like billing due dates. Miss one, apologize, explain what happened, and ask for leniency. Litigation doesn't usually work that way. A statute of limitations can extinguish a claim altogether.

That harsh result is why timing analysis deserves serious attention early. If you wait until a firm has closed its file, a witness has moved on, or electronic records have become harder to collect, the legal deadline problem gets paired with an evidence problem. That combination is avoidable if you act quickly.

What the statute does and doesn't do

A limitations period doesn't tell you whether you were defrauded. It tells you whether the legal system will still let you pursue relief. Those are different questions. I've seen investors focus entirely on proving misconduct while overlooking the separate need to prove the claim was brought on time.

Keep this distinction in mind:

- Merit and timing are separate issues. You can have a strong fraud theory and still face a deadline defense.

- The opening date of the account isn't always decisive. In fraud cases, later events may matter more than the initial sale.

- Silence can be misleading. Many investors hear nothing about timing until the defense raises it aggressively.

Missing the correct deadline can turn a recoverable loss into a procedural dismissal.

That said, limitations law isn't just a trap for investors. Fraud law has long recognized that people who conceal misconduct shouldn't automatically benefit from the passage of time. That's where the next issue becomes critical.

The Discovery Rule A Critical Exception

The most important timing concept in many investor cases is the discovery rule. In plain terms, the clock may start when the investor discovered the fraud, or when the investor had enough information that a reasonable person should have started asking questions. That second part matters. The law often doesn't require full knowledge of every detail before the deadline begins.

Discovery is not the same as certainty

A common mistake is waiting for complete proof. Investors often say, "I suspected something was off, but I didn't know for sure." Courts usually don't require certainty. What often matters is whether there were enough warning signs to put the investor on inquiry notice.

According to FH+H's discussion of fraud limitations, discovery, and continuing wrong issues, multiple jurisdictions use a discovery rule for fraud, but they also impose a reasonable diligence duty. The clock can start when a claimant had enough facts to prompt inquiry, even if the full scheme had not yet been uncovered. That principle holds particular importance in investor-loss cases because fraud can be concealed through layered transactions, and courts distinguish between a single wrongful act with continuing consequences and a series of continuing wrongful acts.

That sounds technical, but the practical takeaway is straightforward. If monthly statements, unexplained losses, unauthorized trades, redemption problems, or shifting explanations gave you reason to investigate, a defense lawyer may argue the clock started then, not later.

What reasonable diligence usually looks like

Reasonable diligence does not mean investors must perform a forensic audit. It does mean they can't ignore obvious red flags indefinitely. In practice, the strongest cases often show that the investor trusted an advisor relationship, received misleading explanations, and did not have fair access to the truth until later.

Useful evidence often includes:

- Account statements and confirms that reveal when irregular activity first appeared

- Emails and text messages showing how the advisor explained losses or delayed disclosure

- Notes from calls or meetings that capture reassurances, excuses, or contradictory stories

- Outside reviews by a new advisor, CPA, or attorney that first exposed the problem

When lawyers analyze these records, side-by-side comparison often matters more than any single document. Tools designed for legal review, including AI document comparison software, can help identify edits, inconsistencies, or shifting narratives across versions of statements, letters, and disclosures.

For investors trying to understand how FINRA handles evidence and timing-related issues, the FINRA discovery guide for investor disputes is also worth reviewing.

What works and what doesn't

What works is building a timeline around when warning signs first became visible and why they did not reasonably reveal the fraud sooner. What doesn't work is assuming "I just found out recently" ends the analysis. In statute of limitations fraud cases, discovery is often the central fight, and it turns on documents, chronology, and credibility.

Different Deadlines for Different Claims

An investor may discover the same misconduct supports several claims, each with its own filing deadline. That is where people get trapped. They hear one limitations period and assume it applies across the board, even though a court claim, a FINRA arbitration, a state securities claim, and a criminal case can run on different clocks.

Some of those clocks are more flexible than they first appear. In fraud matters, the discovery rule and tolling doctrines can extend the window when the misconduct was concealed, but those arguments usually apply differently depending on the claim you are asserting.

A side by side view

| Claim Type | Typical Time Limit | Governing Body / Law |

|---|---|---|

| Civil fraud claim in California | 3 years from discovery | California Code of Civil Procedure § 338(d) |

| Civil fraud claim in New York | 6 years from the fraud or 2 years from discovery, whichever is longer | New York CPLR 213(8) |

| Civil common-law fraud claim in Illinois | 5 years | Illinois limitations rules for common-law fraud |

| Civil fraud claim in Texas | 4 years, subject to discovery rule and fraudulent concealment analysis | Texas law summary discussed later in this article |

| State securities or Blue Sky claim | Deadline varies by state and statute | Review the state-by-state framework for Blue Sky securities laws and investor claims |

| Federal criminal mail fraud or wire fraud | 5 years generally | U.S. Department of Justice guidance on criminal fraud limitations periods |

| Federal criminal mail fraud or wire fraud affecting a financial institution | 10 years | Same DOJ guidance |

The practical point is simple. The right question is not whether fraud occurred in the abstract. The right question is which claims remain available, where they can be filed, and whether the facts support delayed accrual or tolling.

Civil, regulatory, and criminal timelines do different work

Private civil claims are aimed at getting money back. Criminal prosecutions are brought by the government to punish misconduct. Regulatory proceedings may establish wrongdoing, suspend licenses, or impose fines without making the investor whole.

That difference matters because one active government case does not automatically preserve a private investor claim. I often have to explain that a newsworthy SEC or DOJ action may help prove misconduct, but it does not stop every civil deadline from running.

The DOJ guidance also reflects another point that surprises investors. In some criminal fraud cases, later uses of the mail or wires can affect timeliness even if the original lie happened much earlier. That does not mean an investor's civil claim is timely. It means the criminal analysis follows different rules.

Where the real deadline fight usually happens

For investors, the hardest deadline disputes usually arise in civil fraud and state securities claims. One claim may run from the fraud itself. Another may run from discovery. A third may allow tolling if the broker, adviser, or firm concealed the truth well enough that a reasonable investor would not have discovered it earlier.

Those distinctions drive strategy. In a strong case, counsel may plead common-law fraud, statutory securities claims, breach of fiduciary duty, and other theories because each can carry a different limitations analysis. That does not guarantee recovery, but it can preserve options that would be lost if the case were framed too narrowly.

Small wording differences in the statute matter. So do the facts.

How State Laws Impact Your Fraud Claim Deadline

A missed deadline in one state may still be a live claim in another. I see that problem often with investors who relied on general online advice and assumed every fraud case follows the same clock.

The same facts can lead to different filing windows

State law does not treat fraud timing the same way. California generally measures common-law fraud from discovery. New York often allows the longer of a period running from the fraud itself or a shorter period running from discovery. Illinois has its own approach. Those differences can decide whether a case survives a motion to dismiss or never gets off the ground.

The practical point is simple. Deadline analysis is usually tied to the specific claim, the specific state, and the specific facts showing when the investor knew, or should have known, enough to investigate.

That is why the discovery rule matters so much. In concealed misconduct cases, the sale date is only part of the story.

Texas shows how tolling can keep a case alive

Texas is a useful example because it highlights the tension investors face. The basic rule for fraud claims is straightforward, but real disputes often center on whether the claim accrued earlier than the investor reasonably could have recognized the fraud. Texas courts also address fraudulent concealment, which can suspend the running of limitations until the wrongdoing was discovered or should have been discovered through reasonable diligence. The Texas statutes are available through the Texas Constitution and Statutes website.

That creates a real factual fight. Defense counsel will point to account statements, confirmations, emails, and signed forms to argue the warning signs were there all along. The investor's side will focus on what those documents revealed, whether the broker or adviser gave reassuring explanations, and whether a reasonable person in that relationship would have uncovered the truth sooner.

In practice, tolling arguments are strongest when the misconduct was hidden behind complexity, trust, or both.

For a broader look at state securities remedies that may apply alongside common-law fraud, this overview of state Blue Sky laws and investor claims is a useful starting point.

What this means for investors

Do not assume the law of your home state controls. The governing law may turn on where the account was opened, where the adviser worked, where the seller was located, what the contract says, or where the transactions took place. Those choice-of-law questions can change the deadline analysis before anyone reaches the merits.

That is also why early case review matters. A careful lawyer will test more than one claim and more than one state's timing rules, especially where the facts support discovery-based accrual or tolling from concealment.

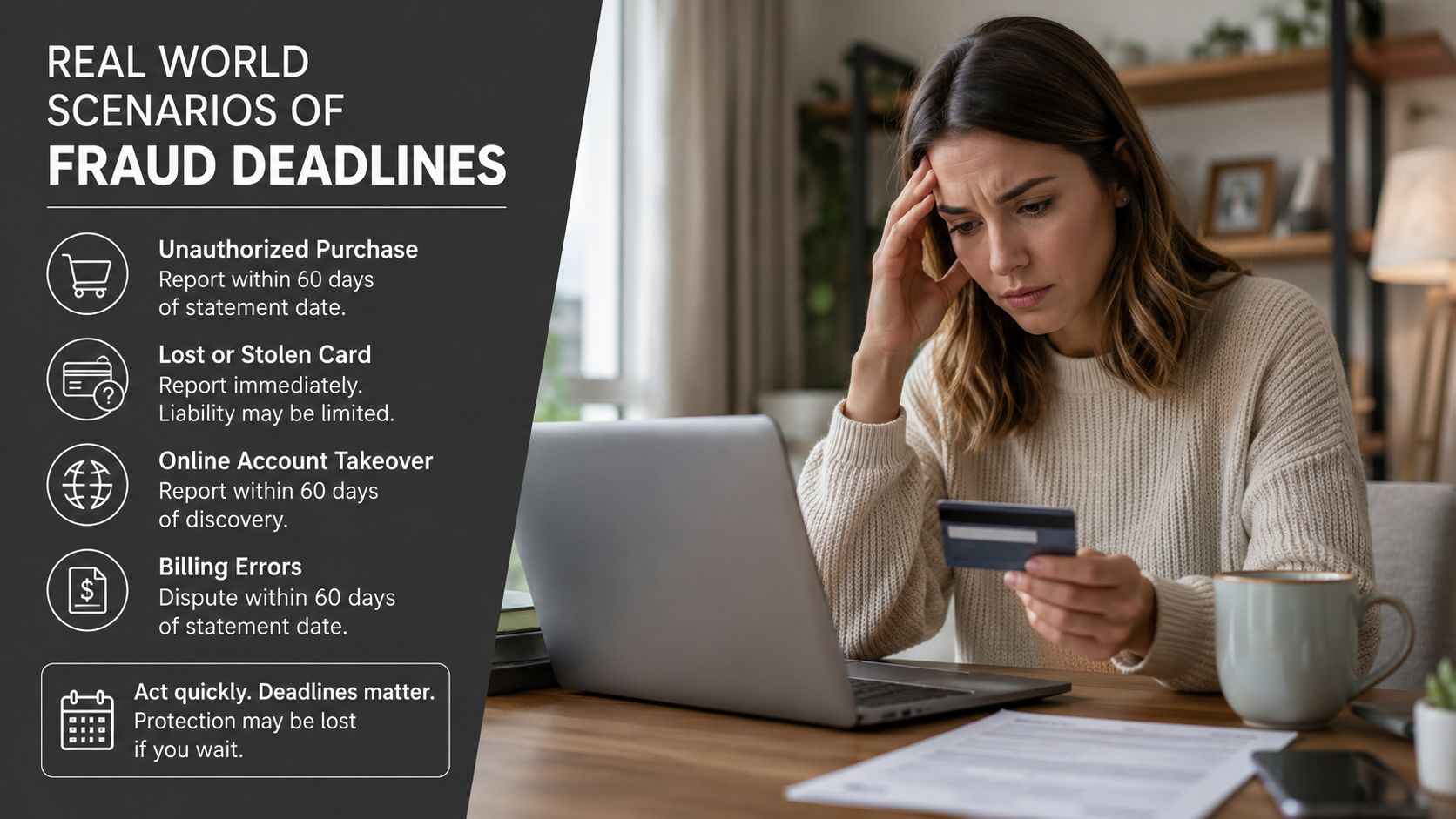

Real World Scenarios of Fraud Deadlines

Abstract timing rules make more sense when you apply them to how investors discover misconduct.

An annuity sale that looked harmless for years

A retiree buys a complex annuity after being told it is safe, liquid, and appropriate for income needs. Years later, the investor learns there are steep surrender restrictions, high internal costs, and features that never matched the stated goals. The investor only understands the mismatch after a different advisor reviews the contract.

In that situation, the sale date matters, but it may not end the inquiry. The legal fight often turns on when the investor had enough information to recognize that the recommendation may have been unsuitable or misleading. If the paperwork was dense, the advisor gave repeated reassurances, and the investor had no reason to distrust those explanations earlier, the discovery issue may support a later accrual date. If warning signs were obvious long before that review, the defense will argue the clock started sooner.

Unauthorized trading hidden in plain sight

An investor receives statements every month but doesn't understand the activity. The broker places trades without approval and justifies losses as active management. Years later, a family member or new advisor notices patterns that don't fit the client's objectives or authorization history.

This is a common deadline problem. Defendants often argue that the statements themselves gave notice. Investors respond that the documents were opaque, the advisor controlled the relationship, and each complaint was met with misleading explanations. The details matter. Courts and panels often focus on whether the statements clearly revealed the wrongdoing or merely contained data that required professional interpretation.

A statement can contain information without fairly disclosing fraud. That distinction matters.

A private placement that kept issuing reassuring updates

An investor puts money into a private deal and receives periodic reports suggesting the project is on track. The reports later prove false or materially incomplete. The investment eventually collapses, and only then does the investor learn that major problems existed much earlier.

Here, concealment is often central. If the issuer or seller used later reports to keep investors calm and discourage scrutiny, the timing analysis may look very different from a case where the risk was fully visible from the outset. The key question is usually not "When did the investment fail?" It is "When did the investor have enough facts that a reasonable person would have investigated and discovered the fraud?"

These scenarios all show the same lesson. The deadline issue lives in the facts, not in a simple calendar calculation.

What To Do Now to Preserve Your Claim

You review your records after an investment falls apart and realize the story changed over time. The account statements were hard to read. The reassurances kept coming. Now the question is urgent. Did the filing clock start months ago, or does the discovery rule or tolling still leave room to act?

That question should be answered with documents, dates, and a legal analysis. Waiting usually makes all three harder.

Five steps that help right away

Collect the entire file. Gather monthly statements, trade confirmations, new account forms, emails, text messages, offering documents, promissory notes, redemption requests, notes from calls, and tax records. Do not pre-screen for what seems important. In fraud cases, one overlooked message often explains when suspicion first arose and whether later concealment delayed discovery.

Write out the timeline while the details are fresh. Note when the investment was pitched, what was promised, when performance changed, when you asked questions, and what answers you received. If you do not know exact dates, put events in order. That chronology often becomes central to any argument about delayed discovery.

Limit informal conversations with the advisor, broker, or firm. Investors often hope one more explanation will resolve the problem. Sometimes it only creates a new record the defense can use to argue that the warning signs were obvious and accepted. Keep communications measured and save everything.

Preserve electronic evidence now. Download portal records, save emails outside the platform, back up text messages, and keep voicemails. Access can disappear after an account is restricted, a phone is replaced, or an employer-controlled email account is shut off.

Get a legal review focused on deadline issues, not just merits. A good case can still be lost if it is filed in the wrong forum or after the wrong deadline. A prompt review can identify whether the stronger argument is fraud, breach of fiduciary duty, negligent misrepresentation, or a securities claim with a different timing rule.

Why acting quickly matters, even if tolling may help

Investors often assume they are out of time because the losses began long ago. That is not always right. In concealed fraud cases, the better question is often when a reasonable investor had enough facts to discover the misconduct, and whether later statements, excuses, or omissions delayed that point.

Texas is a good example. Fraud claims can involve a four-year limitations period, but the start date can become disputed when the defendant hid the misconduct or the investor could not reasonably detect it earlier. Texas courts have addressed those issues in fraud and concealment cases, including decisions collected by the Supreme Court of Texas on its public site. The lesson is practical. Tolling can preserve a claim, but only if the facts are developed early and presented carefully.

That is why speed matters. Memories fade. Portal records disappear. Defendants frame silence as notice.

For investors weighing next steps, speaking with a financial fraud attorney for investment loss cases can help identify the right forum, the strongest tolling arguments, and the documents that matter most before anything is lost.

If you want a plain-English look at how lawyers keep deadline-driven matters organized, this essential legal practice management guide gives a useful overview of chronology, document control, and task tracking.

The most costly assumption is that a claim is probably too old to pursue.

Sometimes a lawyer will confirm that the deadline has passed. That happens. Just as often, the actual analysis turns on discovery, concealment, diligence, and where the claim should be filed. Investors should not make that call on their own.

If you would like a free consultation to discuss the investment loss recovery process in more detail, contact Kons Law. You can also call (860) 920-5181 for a FREE, NO OBLIGATION consultation to discuss your potential rights, deadlines, and recovery options.