You log into your account and see losses that do not match the story you were told. Maybe the account was supposed to be conservative. Maybe your broker said the product was income-focused, low risk, or suitable for retirement funds. Instead, you are staring at sharp declines, illiquid positions, unexplained trading, or a concentration in products you did not fully understand.

Most investors start by asking what the broker did wrong. That is a fair question, but it is often incomplete. In many cases, the better question is why the brokerage firm allowed it to happen.

That is where finra rule 3110 matters. For an investor pursuing recovery, this rule is not just a compliance technicality. It is often the roadmap to proving that the firm failed in its most basic duty to supervise the people and offices that handled your money.

Your Brokerage Firm’s Ultimate Responsibility

A broker rarely works in isolation. Orders are entered through firm systems. New accounts are approved by firm personnel. Sales practices are supposed to be monitored. Customer complaints are supposed to be escalated. When that chain breaks, investors lose money and firms often try to frame the problem as one bad advisor acting alone.

FINRA Rule 3110, the Supervision Rule, was introduced in 2014 as a consolidation of earlier supervisory rules, and it established a unified standard requiring firms to maintain systems designed to supervise associated persons and achieve compliance with securities laws and FINRA rules. In 2023, FINRA proposed amendments aimed at modernizing the rule for remote work arrangements, according to Global Relay’s summary of FINRA Rule 3110.

Why this matters to an injured investor

If your account suffered from unsuitable recommendations, unauthorized trading, excessive trading, or sales of products that never fit your needs, the firm cannot avoid scrutiny by pointing only at the broker. Rule 3110 puts the responsibility on the firm to build and maintain a supervisory system.

That changes the legal posture of a case.

Instead of arguing only that your advisor made bad decisions, a claim can focus on whether the firm had a real system to detect and stop the misconduct. If the answer is no, liability becomes broader and harder for the firm to minimize.

The safety net that should have been there

A proper supervisory system is supposed to catch problems before they become catastrophic. That includes warning signs such as:

- Account activity that does not match your objectives

- Repeated switches among investments that generate commissions

- Concentrated positions in private placements, annuities, non-traded REITs, or other complex products

- Complaints, address changes, fund transfers, or other account events that should trigger review

A failure-to-supervise claim often begins when an investor realizes the firm had multiple chances to catch the problem and did nothing.

That is why investors should stop thinking of supervision as back-office paperwork. It is an investor protection rule. When it fails, the firm may be responsible for the losses that followed.

If you would like a free consultation to discuss the investment loss recovery process in more detail, call Kons Law Firm at (860) 920-5181 for a FREE, NO OBLIGATION consultation.

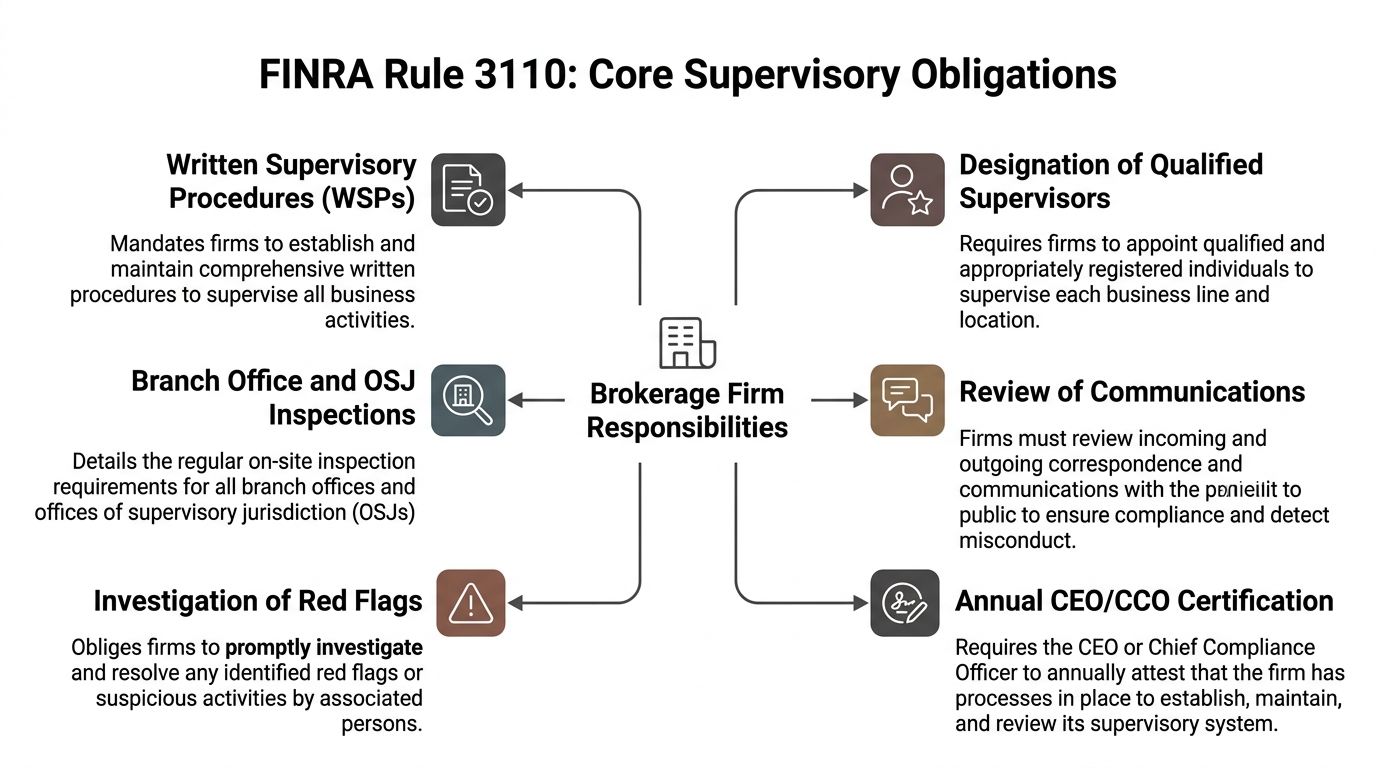

What FINRA Rule 3110 Demands from Brokerage Firms

Think of finra rule 3110 as a building code for brokerage supervision. A firm does not satisfy the rule by saying it values compliance. It needs structure, named responsibility, documented review, and inspections that take place.

Rule 3110 requires member firms to establish and maintain a supervisory system, with final responsibility resting with the firm. That includes Written Supervisory Procedures, or WSPs, identifying supervisors by name, review frequencies, and documentation methods for trading, customer communications, and complaints. It also gives Offices of Supervisory Jurisdiction, or OSJs, heightened duties such as final approval of new accounts and supervision of other branches, and those OSJs must be inspected annually, as described in Scarinci Hollenbeck’s discussion of FINRA Rule 3110.

Written Supervisory Procedures

A firm’s WSPs are supposed to answer practical questions, not just recite the rule.

Who reviews trades. Who reviews customer complaints. Who signs off on account openings. How often review occurs. What records are kept. What happens when a red flag appears.

Weak WSPs often have one of two problems:

- They are too generic. They read well on paper but do not assign concrete responsibility.

- They are not followed. The manual may exist, but the firm cannot show actual reviews, escalations, or corrective action.

For arbitration purposes, that gap matters. A firm that cannot connect its written procedures to real supervisory conduct has a serious problem.

Qualified supervisors and clear accountability

Rule 3110 expects firms to assign supervision to qualified and appropriately registered people. Firms get into trouble when everyone assumes someone else is watching.

A proper structure usually includes:

- Named supervisors for each business line or office

- Defined reporting lines so supervision is not vague

- Separate oversight for supervisory personnel themselves

If the wrong person is assigned, or nobody is specifically assigned, misconduct can run for months or years without meaningful review.

OSJs and why they matter

An OSJ is not just another branch. It is a location with elevated supervisory authority. These offices handle functions such as final approvals for new accounts and oversight of other branches.

That why OSJ failures are important in investor cases. If the office with review authority did not perform its role, the firm’s defense becomes much weaker. In practice, many serious supervision cases trace back to an OSJ that approved activity it did not adequately examine.

Inspections are supposed to test reality

Inspections are where firms prove that supervision exists beyond a policy manual. A real inspection should test what brokers are selling, how records are kept, whether communications are reviewed, and whether customer activity matches risk profiles.

The most important trade-off in supervision is simple. A firm can run lean, or it can supervise well. It cannot ignore oversight and still claim its system was reasonably designed.

A firm that performs inspections only as a formality will miss the same issues that later appear in arbitration. That is often where investors uncover the difference between a compliance program that functioned and one that merely looked acceptable on paper.

Common Supervisory Failures That Cause Investor Losses

Investor losses tied to supervision usually do not come from a single missed step. They come from repeated failures that line up. The broker makes unsuitable recommendations. The branch manager does not question the pattern. Compliance does not escalate the warning signs. The firm later says nobody knew.

That defense often falls apart when the account record is examined closely.

Supervisory deficiencies are one of the most frequently cited violations in FINRA enforcement. Over 40% of FINRA fines in many recent reporting periods have been linked directly to supervision failures, and penalties for Rule 3110 violations can range from tens of thousands of dollars to multimillion-dollar sanctions, according to LeapXpert’s summary of FINRA Rule 3110 enforcement.

Ignored red flags in account activity

This is one of the most common patterns.

The account shows activity that should trigger review, such as frequent switching, unsuitable concentration, or trading inconsistent with the customer’s stated goals. The signs are there in the statements and blotters. Nobody acts.

Common examples include:

- Churning or excessive trading in accounts that should have been managed conservatively

- Overconcentration in one sector, one issuer, or one class of speculative products

- Unauthorized trading followed by after-the-fact explanations

- Losses in products the customer did not reasonably understand

A supervisor does not need a confession to act. The rule expects firms to detect patterns and investigate.

Product approval failures

Some investor losses begin before the first sale. The firm should have vetted the product itself.

That issue comes up often with private placements, non-traded REITs, annuities, BDCs, and other alternatives. If a firm allows brokers to sell a complex or illiquid product without meaningful review, the investor often receives the risk while the firm collects the revenue.

In practice, weak supervision around product sales often looks like this:

- Sales training focused on marketing, not risk

- No meaningful limits on concentration

- No enforcement of suitability standards

- No follow-up when complaints start appearing

Outside business activity can also signal a supervision problem. If you are dealing with a broker who pushed investments away from the firm or blended firm business with outside ventures, issues discussed in this overview of FINRA Rule 3270 may overlap with a Rule 3110 claim.

Weak hiring and branch oversight

Some firms inherit risk and then fail to monitor it. A broker with prior complaints, disclosures, or questionable sales practices should receive closer supervision. If the firm brings that person in and treats supervision as routine, investors absorb the danger.

Many failure-to-supervise cases are predictable. The account activity, the product type, the complaint history, and the office structure all pointed to risk before the losses became severe.

A weak supervisory culture usually leaves clues. Customer complaints are minimized. High-producing brokers are treated differently. Home office arrangements receive less scrutiny than traditional branches. Complex products are allowed to spread faster than the firm’s ability to supervise them.

When those conditions exist, investor losses are often not market accidents. They are the foreseeable result of a firm failing to police its own business.

Real-World Examples of Rule 3110 Enforcement

Regulators treat supervisory failures as serious misconduct because these cases rarely involve harmless paperwork errors. A breakdown in supervision often means the firm failed to stop unsuitable sales, bad communications, self-interested trading, or other conduct that harmed customers.

The enforcement pattern matters even when your arbitration claim is separate from a regulatory case. It shows that the theory is recognized, tested, and taken seriously.

What enforcement actions show investors

A supervisory case usually follows a familiar path. The firm had procedures. The procedures were incomplete, poorly assigned, or ignored. A problem surfaced that should have been caught earlier. Regulators then focused on the system, not just the individual rep.

That distinction is important. Firms often defend arbitration claims by isolating the broker’s conduct. Enforcement history cuts against that approach because FINRA routinely examines whether the firm’s structure made the misconduct possible.

The practical takeaway for arbitration

The best use of enforcement history is not to copy another case. It is to identify the kind of proof that matters in your own matter.

That proof often includes:

- Whether the firm assigned real supervisory responsibility

- Whether the firm reviewed communications and customer complaints

- Whether branch inspections happened on schedule

- Whether exceptions, alerts, or unusual trades were escalated

- Whether the office handling supervision had authority on paper but not in practice

A related issue can arise when brokers participate in away deals or private securities transactions that the firm failed to control. If that fact pattern sounds familiar, this discussion of FINRA Rule 3280 is often relevant alongside Rule 3110.

Why these cases strengthen investor claims

Regulatory actions do not automatically win an arbitration. They do something nearly as important. They validate the core principle that a brokerage firm must supervise actively, document that supervision, and intervene when warning signs appear.

That gives investors a stronger framework. Instead of presenting the loss as a private dispute with one advisor, the claim can be framed as a failure of the firm’s internal controls.

That is often where significant cases gain traction. Arbitrators understand that misconduct becomes much harder to stop when the people tasked with supervision either do not act or never had a functioning process to begin with.

How Rule 3110 Strengthens Your FINRA Arbitration Claim

In arbitration, a firm’s favorite defense is often some version of this: the broker went off script, the firm did not know, and the conduct was outside normal supervision. A strong Rule 3110 claim attacks that defense directly.

Rule 3110(b)(6) requires procedures that bar supervisors from overseeing their own activities. FINRA’s supervision guidance also notes that investors can use these conflict-of-interest prohibitions in claims. In 2025 enforcement sweeps, FINRA fined 22 firms $45 million for supervisory conflicts, with 40% involving self-supervision lapses, according to FINRA’s supervision topic page.

Why systemic negligence is often stronger than a rogue broker story

A broker may have made the recommendation, but firms approve the platform, the office structure, the supervision chain, and the compliance process. If the same person generated business and effectively supervised himself or herself, that is not a personal lapse alone. It is a structural defect.

That matters because arbitrators often respond strongly to failures that look baked into the system. A firm can distance itself from one bad conversation. It has a much harder time distancing itself from defective supervision, conflicted oversight, or an office structure that allowed self-policing.

Conflict issues can be powerful evidence

Self-supervision and dual-role conflicts are especially useful because they are concrete. If a branch manager approved his own activity, or if the firm’s procedures allowed a supervisor to report to himself in practice, the investor has a direct way to show why the misconduct continued.

That can support claims involving:

- Churning

- Unsuitable annuity sales

- Concentrated positions

- Private placement losses

- Elder financial abuse

- Unauthorized trading

In arbitration, strategy matters as much as facts. A case built only around what the broker said may turn into a credibility contest. A case built around documents, role assignments, inspection failures, and conflicted supervision is usually harder for the firm to explain away.

Rule 3110 helps shape discovery

A well-pleaded supervision claim also opens the door to targeted discovery. That is where many cases gain a significant advantage.

Useful requests often focus on the firm’s supervisory system, not just your account file. That includes WSPs, branch review records, exception reports, complaint logs, and documents showing who supervised whom. Investors trying to understand the forum and procedure can also review these FINRA arbitration rules.

A Rule 3110 claim is effective because it changes the narrative. The issue becomes not only what your broker did, but what the firm failed to prevent.

Once that shift happens, settlement discussions often become more serious. Firms know that jurors are not involved in FINRA arbitration, but arbitrators still understand negligence, red flags, and broken supervisory systems. When the documents show that the firm’s controls were weak, the case becomes harder to dismiss as an isolated mistake.

Evidence to Collect for a Failure to Supervise Claim

Investors do not need to prove the whole case before speaking with counsel. They do need to preserve the right material. The best supervision claims are built from ordinary documents that show what you were told, what was sold, and what the firm should have caught.

Under Rule 3110(c), firms must conduct regular periodic inspections of office locations, with OSJs inspected annually and other branches inspected every 1 to 3 years. Requesting inspection logs in discovery can expose oversight gaps, including situations where an uninspected OSJ missed red flags in private placements or annuities, as reflected in FINRA Rule 3110 itself.

Start with your own records

Your personal file is often more valuable than investors expect.

Gather and preserve:

- Account statements showing trades, concentrations, losses, and patterns over time

- Trade confirmations that identify what was purchased and when

- Emails and text messages with the broker or branch personnel

- Notes of phone calls or meetings, even if informal

- Account opening documents and risk tolerance forms

- Marketing materials or product summaries you were given

- Complaint emails or letters you sent to the firm

Do not edit or reorganize these documents in a way that changes dates or context. Preserve them as they exist.

What your lawyer will usually seek in discovery

The strongest Rule 3110 cases usually require internal documents the investor does not already have. Those records help show what the firm knew, who was responsible, and whether the supervisory system functioned.

A practical primer on that process appears in this FINRA discovery guide.

| Evidence Type | What It Can Prove |

|---|---|

| Account statements and confirmations | Trading frequency, concentration, timing of losses, and whether activity fit your objectives |

| Emails, texts, and call notes | What the broker represented, whether risks were disclosed, and whether instructions were ignored |

| New account forms and risk profiles | Whether the recommendations matched your stated age, income needs, liquidity needs, and risk tolerance |

| Product marketing materials | Whether the sales pitch emphasized benefits while downplaying risk, illiquidity, or commissions |

| Customer complaints | Whether the firm had prior notice of problems and failed to respond appropriately |

| Written Supervisory Procedures | Whether the firm had clear supervisory rules and whether those rules assigned actual responsibility |

| Branch inspection logs and reports | Whether required inspections occurred and whether deficiencies were identified or ignored |

| Supervisory review records and exception reports | Whether unusual trading, concentration, or complaint activity was flagged and escalated |

What works and what does not

Some investors think the case turns on proving fraud in the dramatic sense. It often does not. Many successful supervision claims are built on negligence, unsuitable recommendations, ignored warnings, and the firm’s failure to enforce its own rules.

What helps most is consistency.

- Consistent documents beat reconstructed memories.

- Contemporaneous complaints carry weight.

- Risk forms that conflict with the product sold can be highly persuasive.

- Inspection gaps and missing supervision records often speak for themselves.

If the firm cannot produce records showing who supervised the broker, what was reviewed, and when action was taken, that absence can become a central part of the claim.

The goal is not to collect everything possible. The goal is to preserve the documents that connect your losses to the firm’s failure to supervise.

Your Next Steps for Investment Loss Recovery

If you suffered investment losses and the explanation never made sense, do not assume the problem was merely bad market timing. Many losses trace back to a brokerage firm’s failure to supervise sales practices, account activity, branch offices, and the people entrusted with investor funds.

That is the practical force of finra rule 3110. It gives investors a way to examine the firm’s role, not just the broker’s conduct. When supervision failed, the path to recovery often becomes clearer because the claim focuses on firm-wide negligence and broken internal controls.

Act promptly. Preserve account statements, emails, text messages, notes, account forms, and any materials the broker gave you. Do not let the firm frame the issue for you before the records are reviewed carefully.

Legal analysis matters early in these cases. The right review can identify whether the facts support claims based on unsuitable recommendations, unauthorized trading, overconcentration, elder abuse, private placement losses, annuity misconduct, or a broader failure to supervise.

If you would like a free consultation to discuss the investment loss recovery process in more detail, call Kons Law Firm at (860) 920-5181 for a FREE, NO OBLIGATION consultation.

Frequently Asked Questions About Rule 3110 Claims

Can I still bring a claim if I signed an arbitration agreement

Usually, yes. In the brokerage context, arbitration agreements commonly require disputes to be handled in FINRA arbitration rather than court. That does not eliminate your claim. It changes the forum where the claim is heard.

Do I sue the broker, the firm, or both

That depends on the facts, but in many cases the firm is central because Rule 3110 focuses on supervision. The broker may have made the recommendation or placed the trade, but the firm had the duty to supervise, review, inspect, and intervene. In practice, many strong claims are built around both the individual conduct and the firm’s supervisory failures.

What if my losses involved a remote or home office advisor

Remote work does not remove supervisory duties. Firms still must supervise associated persons and office locations under the rule. The structure may look different, but the obligation remains. If a firm expanded remote operations without adapting its supervisory system, that can become part of the case.

Do I need proof that the firm intended to harm me

No. Many failure-to-supervise claims are based on negligence rather than intentional fraud. The key issue is often whether the firm had a reasonably designed supervisory system and whether it followed that system when warning signs appeared.

What if I never filed a written complaint when the problem started

You may still have a claim. Written complaints help, but they are not the only evidence. Account statements, trade confirmations, communications, risk tolerance forms, and internal firm records may still show that the activity was unsuitable or that supervision was deficient.

How do lawyers prove supervision failures if investors do not have internal records

That is where discovery matters. The investor starts with personal records. Counsel then seeks WSPs, inspection logs, supervisory review records, complaint files, account approval records, and other internal documents. Many Rule 3110 cases become much stronger once the firm’s own records are examined.

Is there a deadline to file

Potential deadlines can apply, and timing should be evaluated promptly. The specific analysis depends on the account history, the product involved, when the misconduct occurred, and the applicable arbitration rules and legal claims. Waiting can create unnecessary problems, so investors should have the matter reviewed as soon as possible.

If you believe your losses were caused by unsuitable recommendations, unauthorized trading, churning, private placement misconduct, annuity abuse, elder financial abuse, or a brokerage firm’s failure to supervise, Kons Law can evaluate your situation. Kons Law is a nationwide securities and investment litigation firm focused on recovering money for investors through FINRA arbitration and court actions. To discuss your options, call (860) 920-5181 for a FREE, NO OBLIGATION consultation.