You open your mail or email and see a long settlement notice about a stock you bought, a fund you held, or a company that allegedly misled investors. The notice is dense, the deadlines are easy to miss, and the language makes it sound like the case is already over. For most investors, that's the moment confusion starts.

What matters now is practical action. A class action settlement can create a path to recovery, but it doesn't guarantee money will show up automatically. You need to know what the notice means, what choices you have, what records to gather, and when a separate individual claim may make more sense than staying in the class.

If you want help evaluating that decision, you can speak with Kons Law Firm for a free, no obligation consultation at (860) 920-5181. If you want a quick primer first, this overview of what a class action suit means gives useful background. The rest of this guide focuses on the investor's side of the class action settlement process, not just the court's paperwork.

An Investor's Introduction to Class Action Settlements

A class action settlement is a way to resolve claims for a group of investors who were allegedly harmed by the same misconduct. In securities cases, that often means allegations that a company, brokerage firm, advisor, or other financial actor made misstatements, omitted material information, or engaged in conduct that caused investor losses.

For an injured investor, the class action settlement process usually starts long after the hard part has already happened. You've already taken the loss. The market moved, the account value dropped, or the truth came out after you invested. By the time a notice arrives, lawyers and the court have often been dealing with the case for quite a while.

What the notice is really telling you

The notice usually means a proposed resolution has reached the stage where class members must be informed and given a chance to respond. It is not junk mail. It is also not a demand letter directed at you personally.

Read it for four practical items:

- The definition of the class: This tells you whether your purchases, sales, or holdings fit within the covered group.

- The covered time period: Securities settlements often turn on when you bought or sold.

- Your deadline dates: Missing a claims deadline can be the difference between recovery and no recovery.

- Your choices: Stay in the class, ask to be excluded, or object.

Practical rule: Don't decide based on the headline settlement amount. Your own recovery depends on whether you qualify, whether you file properly, and how the court-approved allocation plan applies to your transactions.

Why investors get tripped up

Many investors assume one of two wrong things. First, they assume the notice means payment is coming automatically. Second, they assume a class settlement is always their best option. Neither is safe to assume.

Sometimes participating in the class is the sensible path. Sometimes an investor with substantial losses, unusual facts, or potential broker misconduct needs a separate analysis. That is especially true when the loss may support a FINRA arbitration claim, an individual fraud claim, or another recovery route outside the class case.

The notice is not the end of the matter. It is the point where your own decisions begin to matter.

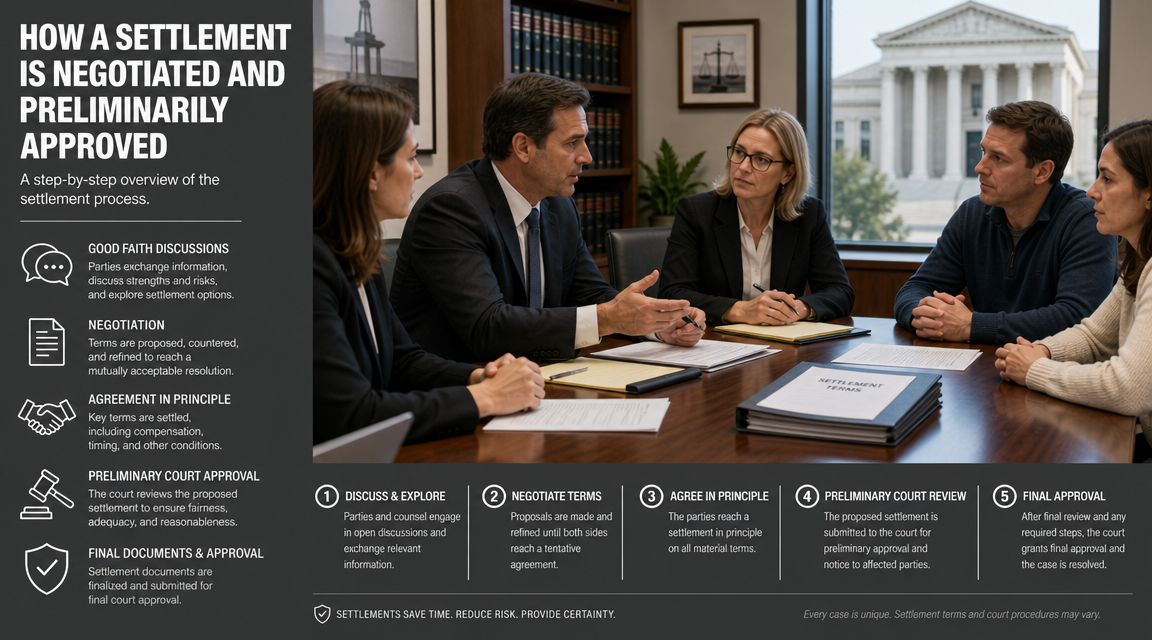

How a Settlement is Negotiated and Preliminarily Approved

Before you ever receive a notice, the case has already gone through litigation, investigation, negotiation, and judicial review. That matters because a settlement doesn't become real just because the parties shake hands.

In securities litigation, the lead plaintiff and class counsel negotiate on behalf of the proposed class. The defense tries to cap exposure, limit admissions, and avoid trial risk. Class counsel tries to obtain a fund or other relief large enough to justify settlement, while also negotiating the release language, the class definition, and the allocation method.

What happens before the notice goes out

The court usually sees a motion for preliminary approval before notice is sent to investors. At that stage, the judge reviews whether the proposed deal appears fair enough to justify notifying the class and moving forward with the formal approval process.

That does not mean the settlement is final. It means the court has allowed the proposal to advance to the next stage.

For investors, that explains an important point. When you receive notice, you are not being asked to vote in a vacuum. The deal has already cleared an initial judicial checkpoint, and the court has allowed notice because the proposal appears serious enough for class members to evaluate.

If you want a broader primer on these cases, this overview of a securities fraud class action is useful context.

Why timing is longer than most investors expect

These cases move slowly. According to ISS Securities Class Action Services reporting on approved settlements in 2022, there were 141 approved monetary class action settlements in 2022 totaling $4.77 billion, with 110 in federal courts and 31 in state courts. Those settlements took an average of 3.6 years from the initial complaint to final judicial approval.

That timing tells investors something practical. A settlement notice is usually the product of a long process, not a fast payout event.

What tends to work in settlement negotiations

From a practitioner's perspective, a settlement is more likely to move when both sides can realistically assess litigation risk. Clear trading data helps. A workable class definition helps. A notice plan and claims structure that the court can approve also help.

What usually doesn't work is assuming the gross settlement number answers the important question. It doesn't. The key investor questions come later. Who qualifies, what proof is required, how losses are measured, and whether filing errors will reduce or eliminate recovery.

A proposed settlement can look substantial on paper and still produce disappointing results for investors who don't fit the claim criteria cleanly or fail to document their transactions.

Your Rights After Receiving a Class Action Notice

Once the notice arrives, your role changes. You now have decisions to make, and each one has consequences. The biggest mistake I see is investors setting the notice aside because they think they can decide later. Deadlines in these cases are strict, and silence is still a decision.

The Federal Trade Commission found that, across a sample of consumer class actions requiring a claims process, the median claims rate was 9% and the weighted mean was 4% of direct notice recipients, according to the FTC's retrospective analysis of class action settlement campaigns. For investors, the lesson is simple. A significant number of people who may qualify never complete the process.

Your three main choices

Most notices give class members three paths.

Stay in the class and file a claim if required.

This is the standard route if you want to seek money from the settlement and don't plan to pursue a separate case.Ask to be excluded, often called opting out.

This preserves your right to pursue your own individual claim, but it usually means you won't recover from the class settlement.Object to the settlement.

This means you remain in the class but ask the court to reject or modify some aspect of the deal, such as the settlement terms, fees, or plan of allocation.

A separate issue sometimes arises in matters that overlap with consumer claims or other forms of misconduct, such as privacy failures. If that sounds familiar, this discussion of data breach class actions may help you understand how notice and claims issues can look in related contexts.

Your Options as a Class Member

| Your Action | What It Means | Can You Get Money from This Settlement? | Can You Sue Individually Later? |

|---|---|---|---|

| Stay in the class | You remain bound by the settlement if approved | Usually yes, if you meet the requirements and file properly when a claim is required | Usually no, for released claims |

| Opt out | You exclude yourself from the class settlement | No | Yes, subject to your own claim's merits and deadlines |

| Object | You stay in the class but challenge some part of the proposed settlement | Potentially yes, if the settlement is approved and you otherwise qualify | Usually no, unless you separately opt out |

How to think about the choice

If your losses are modest and your facts match the class allegations, staying in the class often makes sense. If your losses are large, your account activity is unusual, or your damages may have been caused by a broker or advisor rather than only by the issuer's public statements, you should pause before doing nothing.

Objecting can be appropriate, but it isn't a substitute for opting out. Investors confuse those two all the time. An objection says, "I want the court to review this deal." An exclusion says, "I don't want to be bound by this deal."

Missing the opt-out deadline is often irreversible. If you think you may want an individual case, get that analyzed before the exclusion date passes.

Filing Your Claim to Secure Your Payout

This is the part of the class action settlement process where many valid claims fall apart. Investors assume eligibility is enough. Usually it isn't. In many settlements, you must submit a claim package, and the details matter.

The practical question isn't whether a settlement exists. It's whether you've done what the settlement requires to get paid. The George Washington University guidelines material discussing class settlements and claims-made structures highlights that many class members do not receive money automatically and that the key question is what you must do to recover.

What the claims administrator usually needs

The claims administrator is the third party that receives, reviews, and processes claim forms. In a securities case, a Proof of Claim often asks for transaction-specific information.

Gather these records early:

- Monthly brokerage statements: These often show holdings, purchase dates, sale dates, and account ownership.

- Trade confirmations: These can help if the claim form asks for exact transaction details.

- Account opening or ownership records: Useful if the account is in a trust, IRA, joint name, or estate.

- Any prior correspondence about mergers, ticker changes, or reorganizations: Those events can affect how transactions are reported.

If your losses involve a brokerage recommendation or account handling issue in addition to a public-company case, this article about a class action lawsuit against Vanguard shows how investors often need to separate class-wide allegations from their own account-specific facts.

Common filing mistakes

Most rejected or delayed claims are not rejected because the investor was dishonest. They are rejected because the submission was incomplete, inconsistent, or undocumented.

Watch for these problems:

- Using summary numbers only: Administrators often need transaction-level detail, not just a total loss figure.

- Leaving out sales or retention data: In securities settlements, when you sold can matter as much as when you bought.

- Submitting illegible or partial records: Missing pages create avoidable review issues.

- Ignoring deficiency notices: If the administrator asks for clarification and you don't respond, the claim can stall or fail.

A practical filing routine

Use a simple process.

First, read the claim form once without filling it out. Mark every place where a document is needed. Next, create one file or folder for all account statements and trade confirmations for the relevant period. Then complete the form slowly, matching each entry to the records in front of you rather than relying on memory.

Case handling note: If your records don't line up neatly because of transfers between firms, inherited accounts, or advisor-managed trades, get help before filing. Those fact patterns often need explanation, not just paperwork.

Keep copies of everything you submit, including the final signed form and proof of transmission.

Final Court Approval and Fund Distribution

Investors often think settlement means payment is imminent. It usually doesn't. A proposed settlement still has to survive final judicial review, and even after approval there can be administrative and appellate delays.

In U.S. class action practice, funds are not released immediately after agreement. The court must grant final approval after determining the settlement is fair, reasonable, and adequate, and only then can checks or other payments issue, subject to any appeals, as explained in this overview of the stages of a class action settlement.

What happens at final approval

At the final approval hearing, the judge considers the full record. That can include the settlement terms, the notice process, objections from class members, requested attorney fees, and the proposed allocation method.

If the court grants final approval, that is a major milestone. But it still may not be the last one. If an objector appeals, distribution can slow down while the appeal is resolved or while the parties address the issue.

Why the gap between approval and payment can feel long

After final approval, the administrator still has work to do. Claims must be reviewed. Deficiencies must be addressed. Ineligible claims must be screened out. Eligible claims must then be calculated under the approved plan.

Investors should expect this phase to take time, especially when the settlement covers a large class or complex trading histories.

A realistic way to think about distribution is this:

- Court approval opens the door to payment

- Claims administration determines who gets paid

- Appeals or unresolved objections can delay the process further

What you can do during the waiting period

You don't control the court calendar, but you can still protect your claim.

- Monitor your mail and email: Administrators often send follow-up requests or deficiency notices.

- Keep your address current: Payment problems often start with stale contact information.

- Save your submission records: If there is a dispute later, your proof of timely filing matters.

Payment timing is often frustrating, but the delay usually reflects process, not necessarily a problem with your individual claim.

Understanding Fees Costs and Tax Implications

The settlement amount announced in a press release or notice is the gross fund, not the amount each investor will pocket. Before money reaches claimants, the court may approve attorney fees, litigation expenses, and administration costs. Then the remaining net fund is distributed under the plan of allocation.

The payout math is rarely one-size-fits-all. As explained in this discussion of how class action settlements and payout structures work, distributions are made under a court-approved plan and may be loss-weighted rather than equal-share. The same gross settlement can produce very different net recoveries depending on claim volume, costs, and documentation standards.

Where the money goes before distribution

Investors should read the fee and allocation sections of the notice carefully. Those sections usually identify the categories of deductions and describe how the remainder is allocated.

Common deductions include:

- Attorney fees: These are subject to court approval, not set solely by private agreement.

- Case expenses: Litigation costs can include filing costs, expert work, notice expenses, and document management.

- Administration costs: The administrator must process claims, review records, communicate with class members, and distribute funds.

That doesn't mean a settlement is unfair. It means the headline number is only the starting point.

Why two investors can recover very different amounts

Even if two investors each file on time, their recoveries may differ because the plan of allocation often turns on transaction history, recognized loss calculations, holding periods, and available proof.

One investor may have clean brokerage records and trades that fit the strongest damages window. Another may have mixed transactions, missing records, or trades outside the most compensable period. Same settlement. Different result.

Settlement economics are driven by the allocation plan, not by the assumption that every claimant gets an equal slice.

Tax treatment needs individual advice

Tax questions come up in almost every settlement. The answer depends on the nature of the recovery and how it is characterized. Some portions may be treated differently from others, and account type matters too.

For that reason, it's smart to speak with a tax professional before spending the proceeds. If you're already dealing with a broader tax dispute or collection issue connected to your finances, these proven IRS negotiation strategies offer a useful overview of how tax matters are approached strategically. For settlement-specific tax treatment, though, your own accountant or tax lawyer should review your facts.

When You Should Contact an Attorney for Your Case

Some investors can read the notice, file the claim, and move on. Others shouldn't rely on the class process alone. The hard part is knowing which category you fall into.

You should consider individual legal advice if your losses are substantial, your account was actively managed by a broker or advisor, or your facts don't fit neatly into the class allegations. A securities class action usually addresses common issues affecting many investors at once. It may not address unsuitable recommendations, concentration, unauthorized trading, misleading sales practices, or account-specific fiduciary breaches.

Situations that call for a closer review

An attorney should review your matter if any of these apply:

- Large losses: A major loss may justify analyzing whether opting out and pursuing an individual claim provides a greater advantage.

- Broker or advisor involvement: If your loss was tied to recommendations, supervision failures, or misconduct in your account, the class may address only part of the problem.

- Unclear documentation: Trust accounts, inherited accounts, managed accounts, and transferred positions often require more than a standard claim form.

- Deadline pressure: If the opt-out deadline is approaching and you still don't know whether to stay in, waiting is risky.

Why personalized review matters

A lawyer can compare the class settlement path against other recovery options, including individual litigation or FINRA arbitration where appropriate. That review should focus on your account statements, trade history, communications, and the source of the loss.

In practice, record quality often shapes strategy. Organized statements, confirmations, and advisor correspondence make evaluation faster and more accurate. If you need help understanding how legal teams convert raw records into usable case files, this overview of Meowtxt legal transcription is a practical example of how documentation gets turned into reviewable evidence.

Kons Law handles investor-loss matters involving brokerage firms, financial advisors, and related financial misconduct, including class action and individual recovery analysis. The right path depends on the facts, not the label attached to the notice.

If you're not sure whether to remain in the class, opt out, object, or pursue a separate claim, get that advice before the deadline makes the decision for you.

If you would like a free consultation to discuss the investment loss recovery process in more detail, contact Kons Law or call (860) 920-5181 for a FREE, NO OBLIGATION consultation.