You open an account to preserve retirement savings, pay for a child's education, or invest with professional help. Then the statements start changing in ways you didn't expect. Holdings appear that you don't recognize. Trades seem too frequent. The explanation from your broker or advisor sounds polished, but it doesn't answer the basic question that matters most. Who, exactly, was handling your money, and what were they allowed to do?

That question usually leads back to the same place: the securities firm behind the advisor, platform, or account. For many investors, the firm stays in the background until something goes wrong. But when losses follow unsuitable recommendations, unauthorized trading, excessive commissions, or poor supervision, the firm often becomes central to any recovery effort.

This industry is enormous. The U.S. securities industry managed assets exceeding $50 trillion in 2023, with approximately 85 million retail brokerage accounts active, according to the SEC's 2025 release. That scale is one reason the rules are so dense and investor protections matter so much.

If you're trying to understand what is a securities firm, don't think of it as an academic definition. Think of it as the legal and operational entity that may have sold the investment, approved the recommendation, processed the trade, held the account, or failed to supervise the person who dealt with you. Firms differ in structure, incentives, and duties. Those differences often explain why an investor was exposed to unnecessary risk.

For readers who want a broader financial services context before looking at the legal issues, Algomizer's financial services firm overview is a useful starting point.

When investors come in after losses, they often know the advisor's name but not the firm's role. In many cases, the firm's structure explains the harm better than the sales pitch ever did.

Introduction Understanding the Firm Behind Your Investments

A securities firm is a regulated business that deals in securities. That can include stocks, bonds, mutual funds, ETFs, options, private placements, annuities tied to securities, and other investment products. Depending on its license and business model, the firm may execute trades for customers, trade for its own account, raise capital for companies, custody assets, or supervise the professionals who recommend investments.

Think of the firm as the marketplace operator

Most investors focus on the person they spoke with. Legally, that's only part of the picture. The firm often provides the platform, the compliance department, the product menu, the compensation structure, and the supervisory system. It may also write the procedures that determine what gets approved and what gets ignored.

A simple analogy helps. A securities firm can function like a highly regulated marketplace for financial products. In one transaction, it may act as your agent, trying to execute your order. In another, it may act as a principal, selling from inventory or taking the other side of a transaction. Those are different roles, and they create different incentives.

Why the distinction matters after losses

As of 2024, there were 3,249 FINRA-registered broker-dealers in the United States, and those firms generated $641.0 billion in gross revenues, according to the SIFMA Fact Book. That isn't just market trivia. It shows how central these firms are to the movement of investor money.

When people ask what is a securities firm, they're usually really asking one of these questions:

- Who approved this recommendation

- Who earned the commission or fee

- Who supervised the broker or advisor

- Who may be legally responsible for the loss

Those are the right questions.

Practical rule: If you suffered investment losses, identify the firm before you argue about the product. The same investment can lead to very different legal claims depending on who sold it and in what capacity.

Decoding the Core Role of a Securities Firm

The core job of a securities firm is to connect capital with transactions. Sometimes that means matching buyers and sellers in the secondary market. Sometimes it means helping a company issue securities in the primary market. Sometimes it means recommending investments to retail customers through brokers or advisors.

That broad description sounds harmless. In practice, the details matter.

Broker, dealer, or both

A broker acts for a customer. The broker's role is to facilitate a trade or recommendation for the investor's account.

A dealer trades for the firm's own account. In that role, the firm may hold inventory, make markets, or sell products in which it has a direct financial interest.

A broker-dealer combines both functions. That combination is common. It's also where many investor disputes begin, because a firm can move between roles in ways clients don't fully understand.

Consider this the most straightforward explanation:

| Role | What the firm is doing | Main investor concern |

|---|---|---|

| Broker | Acting as intermediary for your trade | Whether the recommendation or execution was appropriate |

| Dealer | Acting for its own account | Whether the firm had a conflict in pushing the product |

| Broker-dealer | Wearing both hats depending on the transaction | Whether you were told which role the firm was playing |

What firms actually do day to day

A securities firm may handle several functions at once:

- Trade execution: Buying or selling securities in response to customer instructions.

- Investment recommendations: Suggesting products, strategies, or asset allocations.

- Underwriting: Helping companies issue new securities.

- Market making or inventory sales: Trading as principal.

- Supervision and compliance: Monitoring registered representatives and account activity.

- Custody or account administration: Holding assets directly or through related entities.

For investors, the legal issue usually isn't whether the firm offered many services. It's whether the way those services were delivered exposed the client to avoidable harm.

What works and what doesn't

What works is transparency. A client should know who the firm is, how the representative is licensed, how the account is paid for, and whether the recommendation benefits the firm in a way that creates tension with the client's interests.

What doesn't work is blurred language. Many investors hear “advisor,” “wealth manager,” or “financial consultant” and assume the person must always act in their best interest. That assumption can be costly. Titles can be broad. Duties are not.

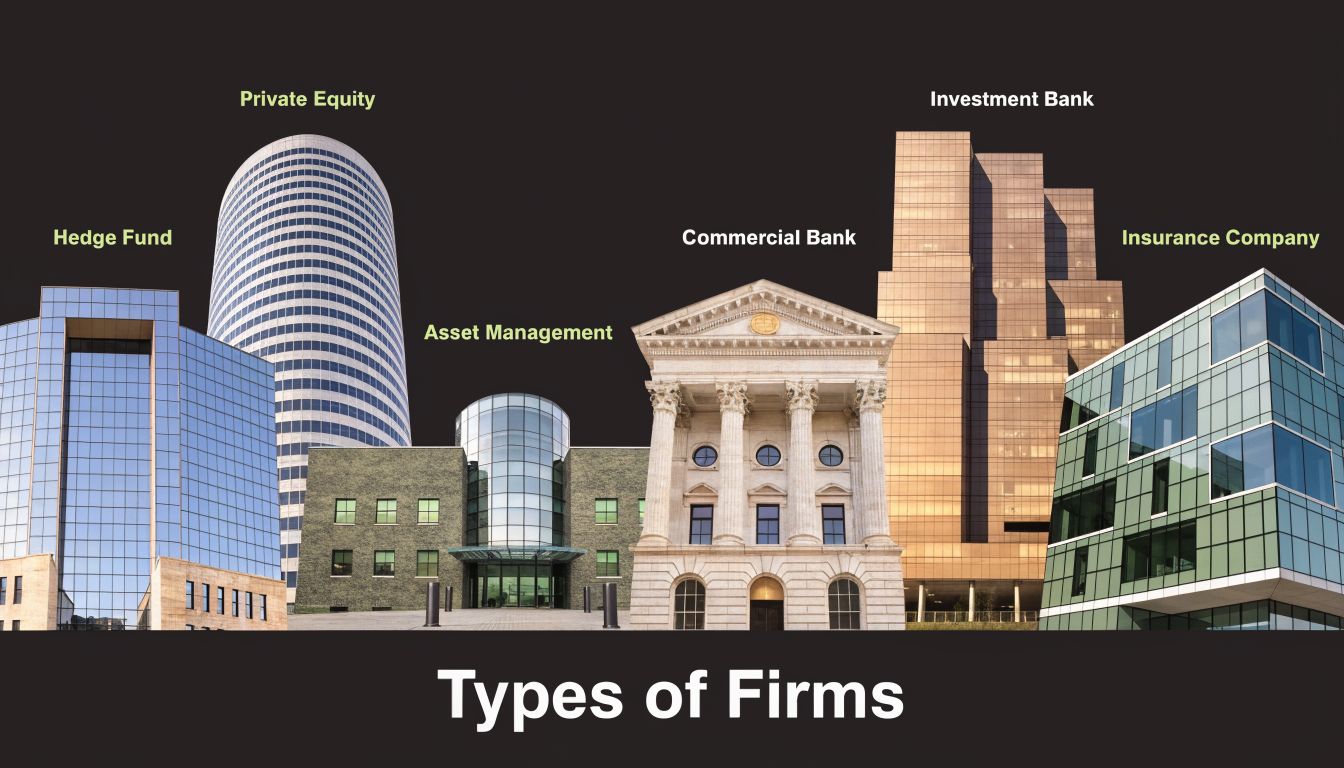

The Main Types of Securities Firms You Will Encounter

Investors usually encounter four categories of firms. Sometimes one company fits more than one category. That overlap is where confusion starts.

Broker-dealers

These are the firms most retail investors know best. They employ or affiliate with registered representatives who sell securities, place trades, and recommend products.

The business model often mixes commissions, product incentives, platform fees, and asset-based charges. That doesn't mean every broker-dealer acts improperly. It does mean compensation can shape recommendations.

The risk is clearest when a firm pushes proprietary or higher-commission products. FINRA reported 1,247 disciplinary actions against firms in 2024 for supervisory failures, often tied to high-risk product sales and oversight problems, as described in the referenced industry material. If you want a focused comparison of legal differences in these channels, this discussion of investment advisor vs broker-dealer is useful.

Investment banks

Investment banks typically work on capital raising, underwriting, mergers, and corporate transactions. Individual investors may think they have nothing to do with this world. That's not always true.

Retail losses can trace back to products created, structured, or distributed through investment-banking channels. The investor may never speak to the underwriting desk, but the product reaches the account through affiliated brokers or selling agreements. The conflict can arise when product distribution outruns product suitability.

Registered investment advisors

An RIA generally provides advisory services for a fee. In plain terms, the client pays for advice rather than for a series of sales transactions. That model often sounds safer to investors, and sometimes it is. But fee-based arrangements can still produce harmful conduct, including overconcentration, failure to diversify, private placement recommendations, and conflicts involving outside business activities.

An advisory label shouldn't end your analysis. You still need to ask what the person recommended, how they were paid, and whether the account was monitored responsibly.

Clearing firms

Clearing firms are less visible, but they matter. They process trades, carry accounts, issue statements, and handle back-office functions for introducing firms.

Many investors don't learn the clearing firm's name until they review statements after losses. In some cases, the clearing firm is mostly administrative. In others, its records become important evidence. They can help show trading frequency, commissions, concentration, and the timeline of disputed activity.

A quick comparison of risk points

| Firm type | How investors usually encounter it | Typical pressure point |

|---|---|---|

| Broker-dealer | Through a broker or “advisor” | Product sales incentives and supervision failures |

| Investment bank | Through structured offerings or affiliated sales channels | Product complexity and distribution conflicts |

| RIA | Through fee-based planning or account management | Fiduciary breaches, concentration, poor monitoring |

| Clearing firm | On statements and account documents | Record trail, account handling, operational issues |

The firm's label matters less than its conduct. A sophisticated name doesn't protect an investor from unsuitable sales practices.

Services Offered and the Legal Duties Attached

The same firm may execute trades, recommend investments, manage assets, and custody funds through affiliates. Each function carries legal consequences. Investors often lose sight of that because the relationship feels personal. The law looks at the role being played.

Common services and the duty question

A securities firm may offer:

- Execution-only services: The firm processes trades you direct.

- Recommendation-based brokerage: A broker suggests products or strategies.

- Advisory management: An advisor manages assets or gives ongoing advice for a fee.

- Retirement and income planning: The firm recommends annuities, REITs, alternatives, or income products.

- Alternative investment access: The firm places clients into private placements or non-public offerings.

Each service raises a different question. Was the firm carrying out an instruction, or was it steering the client into a product?

Suitability and fiduciary duty are not the same

This is one of the most important distinctions in any investment loss case.

A suitability framework asks whether a recommendation fit the client's profile in a general sense. That includes factors like age, objectives, risk tolerance, liquidity needs, and investment experience.

A fiduciary duty is more demanding. It requires loyalty and care. The advisor must place the client's interests ahead of the advisor's own.

Here's the practical difference:

| Standard | What it asks | Real-world effect |

|---|---|---|

| Suitability | Was this recommendation appropriate for this client category | A firm may defend a product as acceptable even if it was expensive or conflict-laden |

| Fiduciary duty | Was this advice in the client's best interest with loyalty and due care | The advisor must account for conflicts and cannot favor the firm's economics over the client |

A retirement investor who needs liquidity may be sold a product that a broker later argues was “suitable” because the investor wanted income and had moderate risk tolerance. That same recommendation may still be challenged if the product carried steep commissions, long lockups, or risks that were inconsistent with the client's real needs.

For a closer look at how these claims are analyzed, this overview of what is a breach of fiduciary duty lays out the core legal theory.

What works in practice

Good firms document the client's objectives carefully, explain product limits clearly, and revisit recommendations when circumstances change. They don't rely on broad boilerplate to justify concentrated or illiquid investments.

Poor practice looks different:

- Profile inflation: The investor is labeled more aggressive than they really are.

- Liquidity mismatch: Long-term, hard-to-exit products are sold to people who may need access to cash.

- Compensation-driven advice: The product chosen pays the firm more than available alternatives.

- Static supervision: No one reevaluates whether the recommendation still fits the client.

If the paperwork says you wanted speculation, but your real goal was preserving retirement income, the paperwork isn't the end of the case. It may be the beginning of it.

Common Misconduct and Investor Red Flags

Most investor claims don't arise because markets fell. They arise because someone used the market decline, product complexity, or industry jargon to cover conduct that shouldn't have happened in the first place.

Churning and excessive trading

Churning happens when a broker trades excessively to generate commissions rather than to serve the client's interests. You may not notice it right away if the account statements are dense or the broker keeps saying the strategy is “active.”

Red flags include:

- Frequent in-and-out trading: Positions open and close without a clear investment thesis.

- High commission charges: Fees keep appearing even when the account isn't making real progress.

- Confusing explanations: The broker talks about timing and opportunity but can't explain why so many trades were necessary.

- Account fatigue: You stop reading statements because the volume is overwhelming.

Unauthorized trading and account activity

Unauthorized trading is exactly what it sounds like. The firm or broker placed trades without your approval, or beyond the authority you gave.

Watch for these signs:

- You see securities you never discussed

- Trade confirmations arrive after the fact

- Money moves between positions without clear consent

- You're told the trade was “housekeeping” or “routine”

If an investor reports this early and the firm minimizes it, that response can become important evidence.

Unsuitable recommendations

Unsuitability claims are common in cases involving retirees, concentrated positions, illiquid products, and alternatives. The product may be legal and real. The problem is that it never belonged in that client's account.

Examples often involve:

- Non-traded REITs

- Private placements

- Complex annuities tied to securities features

- Structured products

- Speculative sector concentration

The sales pattern matters. If the recommendation was described as safe, income-producing, conservative, or appropriate for retirement preservation, compare that language against the actual risks and restrictions.

Misrepresentation and omission

Sometimes the core problem is not the product itself but what the investor was told. A statement can be misleading because of what it includes or what it leaves out.

A broker may describe potential income and skip over illiquidity. A sales presentation may emphasize downside protection while failing to explain caps, conditions, or issuer risk. In these cases, notes, emails, text messages, and offering materials often matter as much as the account statement.

For investors trying to identify whether misconduct may be present, these examples of broker misconduct claims track many of the fact patterns seen in arbitration.

Newer risk areas

Crypto-linked products, app-based trading tools, and algorithmic recommendations have created newer versions of old problems. The label changes, but the legal themes stay familiar: disclosure, authorization, suitability, supervision, and conflict.

If a firm promotes something as original or new, that doesn't answer whether it was appropriate for you. It only tells you how the product was marketed.

Review the monthly statements, confirmations, emails, text messages, account forms, and notes from calls. Investors often have more proof than they think.

Charting Your Path to Recovery After Investment Losses

You open your account statement after a call where the broker said the losses were temporary, market-wide, or part of the plan. Then you see something different. The account is down sharply, the holdings are not what you thought you owned, and the explanation still does not match the paperwork.

At that point, recovery becomes a legal and procedural question, not just an investment question. The right path depends on the firm involved, the agreements tied to the account, the records available, and whether the conduct points to negligence, misrepresentation, unauthorized trading, unsuitable recommendations, or supervision failures.

For many investors, the first forum is FINRA arbitration. Most brokerage account agreements require it, and firms rely on those provisions. Arbitration is still a formal case. It begins with a statement of claim, proceeds through document exchange and motion practice, and often ends with a recorded hearing where witnesses testify under oath and arbitrators decide liability and damages.

Court litigation remains important in the right case. Some disputes belong there because the responsible party is outside the brokerage agreement, the facts involve related fraud or fiduciary issues, or the available claims are broader than what arbitration will fully address. Choosing between arbitration and court is a legal judgment call. It turns on who can be sued, what contracts control, and which forum gives the investor the stronger position.

Timing matters.

Investors often hurt their own cases by waiting too long, accepting a vague verbal explanation, or letting records scatter across phones, inboxes, and file drawers. Before arguing with the firm, gather the documents that show what was recommended, what was purchased, what risks were disclosed, and what authority the broker had.

Focus on these records:

- Monthly statements and trade confirmations

- Account opening documents and suitability forms

- Emails, text messages, and notes from calls or meetings

- Prospectuses, offering memoranda, and marketing materials

- Any written complaint sent to the firm and any response

A securities attorney uses those materials to build the timeline, measure damages, and identify claims the firm may never volunteer. If you want context on that role, this explanation of what a securities lawyer does in investor loss cases is a useful starting point.

Kons Law is one example of a firm that handles FINRA arbitration and court actions involving brokerage and investment-related losses. Law firms that focus on these matters also depend on public trust and clear communication to attract more legal clients, which is one reason investor reviews and case histories can be worth reading as you evaluate counsel.

When You Should Contact a Securities Attorney for Help

You should contact a securities attorney when the explanation you're getting doesn't match what happened in your account. That includes sudden losses in “safe” investments, trades you didn't authorize, a concentration you never agreed to, or a product that was described in one way and behaved in another.

Large firms have compliance departments, counsel, supervisors, and established response procedures. Individual investors usually have statements, memory, and frustration. That imbalance is real. A securities attorney helps level it by identifying viable claims, framing the facts properly, obtaining the right records, and presenting the case in the forum that applies.

You don't need to know the legal label before calling. You don't need to decide on your own whether the problem is churning, unsuitability, unauthorized trading, negligence, or breach of fiduciary duty. A lawyer's job is to sort that out. If you want a clearer sense of that role, this explanation of what is a securities lawyer is worth reviewing.

There's also a practical point clients often overlook. Firms pay attention to documentation, timelines, and presentation. Investors should too. That's one reason law firms invest in communication systems and public trust signals. For firms looking to attract more legal clients, reputation management has become part of how prospective clients judge whether a practice is organized and responsive enough to handle a complex financial dispute.

A delayed review can cost an investor leverage. Statements, trade records, and communications tell the story best when they're gathered early.

If you would like a free consultation to discuss the investment loss recovery process in more detail, call Kons Law Firm at (860) 920-5181 for a FREE, NO OBLIGATION consultation.

If you believe a brokerage firm, financial advisor, or investment advisory firm caused your losses through misconduct, negligence, or fraud, Kons Law offers free consultations for investors nationwide and handles claims through FINRA arbitration and court proceedings.