If you have sold investment property and someone is urging you to move quickly into a fractional replacement property, slow down. A tenants in common 1031 exchange can be lawful and useful, but it is not simple, and it is not risk-free.

That matters most when the recommendation comes from a broker, advisor, or sponsor who focuses primarily on tax deferral and barely mentions structure, restrictions, liquidity, co-owner conflict, or securities liability. Many investors first hear about a TIC only after they are under deadline pressure. That is a dangerous time to make a permanent decision.

Introduction to Tenants in Common 1031 Exchanges

A tenants in common 1031 arrangement is a form of co-ownership. Multiple investors hold undivided interests in the same real property. Each investor owns a separate fractional share rather than shares of a company that owns the property.

That structure gained traction after the IRS issued Revenue Procedure 2002-22, which provided the framework for TIC ownership to qualify as replacement property in a 1031 exchange and allowed up to 35 investors to co-own fractional interests while preserving tax-deferral treatment, as described in this discussion of what is a tenants-in-common structure.

Why investors are drawn to TICs

The sales pitch is easy to understand.

You sell a property. You want to defer taxes under Section 1031. You do not want to manage another building yourself. A sponsor offers a fractional interest in a larger property and tells you the structure can deliver passive ownership, diversification, and tax deferral.

Those are the headline benefits. They are also the beginning of the analysis, not the end.

Where investors get into trouble

A TIC is not just a property decision. In many offerings, it is also a securities law problem if the investment was sold through a broker-dealer or financial advisor under a recommendation process that was unsuitable, misleading, incomplete, or conflicted.

The practical risk is not limited to whether the building performs. Investors also face risk from:

- Bad structuring that can jeopardize exchange treatment

- Weak disclosure about fees, debt, management limits, and exit options

- Illiquidity if the investor later needs cash

- Co-owner conflict when interests diverge

- Broker misconduct if the product was pushed on someone who should never have been in it

A tenants in common 1031 investment should be evaluated as both a tax structure and an investment product. Investors who review only the tax angle may miss the litigation angle.

Many articles stop here. They explain the deferral concept and move on. That leaves out the part that matters when money has already been lost. How the TIC was sold, what was disclosed, and whether the structure was appropriate often drives recovery claims.

Understanding IRS Eligibility Rules for TIC 1031 Qualification

The IRS did not create a broad safe harbor for every co-ownership arrangement. It set boundaries. Revenue Procedure 2002-22 establishes 15 conditions that a TIC structure must satisfy if the parties want the IRS to treat each owner as holding real property directly rather than as part of a partnership. That summary appears in this overview of tenancy in common rules under Rev. Proc. 2002-22.

That distinction controls everything. A TIC interest can qualify as like-kind real property. A partnership interest generally cannot.

The rules that matter most in practice

Some requirements are technical. Others go to the heart of whether the arrangement looks like true co-ownership or an operating business.

The key issues typically include:

- Direct title ownership. Each co-owner must hold direct title as a tenant in common under local law, either personally or through a disregarded single-member entity.

- No more than 35 co-owners. The IRS drew a line at 35 co-owners.

- No partnership tax return. Owners report their own items individually rather than filing as a partnership.

- Transfer and encumbrance rights. Owners generally need independent rights to transfer, partition, or encumber their own interests.

- Pro rata economics. Income, expenses, and sale proceeds are expected to follow ownership percentages.

- Investment-only posture. The arrangement cannot drift into active business operations.

The most serious TIC failure is partnership recharacterization. If the IRS decides the co-owners are really operating as a partnership, the 1031 deferral can collapse and the deferred gain can become immediately taxable.

That is not an abstract drafting concern. It goes directly to how the deal is run.

Why management terms create problems

Investors assume the sponsor can solve everything through centralized management. That instinct creates one of the biggest compliance traps.

Rev. Proc. 2002-22 limits management arrangements. The offering cannot look excessively like an enterprise run through a manager while owners function like members of a business entity. Long-term or excessively permanent or operational management can make the arrangement resemble a partnership more than passive co-ownership.

Voting rights matter too. If the documents require broad collective approvals on key actions in a way that mirrors entity governance, the IRS can question whether the TIC has substance.

What investors should read before signing

Most investors are handed a stack of documents under severe time pressure. The tax focus tends to crowd out basic legal review.

Read these documents closely:

| Document | Why it matters |

|---|---|

| TIC agreement | Defines ownership rights, voting, transfers, expense allocation, and restrictions |

| Property management agreement | Can reveal management terms that create IRS risk |

| Debt documents | Show lender controls, reserves, and default triggers |

| Offering materials | Describe risks, fees, conflicts, and assumptions |

| Subscription package or sponsor documents | May frame the investment as a security with limited liquidity |

If the sponsor delivered a private offering package, investors should understand what a private placement memorandum means in an investment dispute before assuming disclosure was adequate.

What does not work

Several patterns repeatedly create trouble:

- Entity-like governance

- Restrictions excessively tight that owners do not control their own interests

- Management arrangements that look excessively permanent or operational

- Marketing that promises passive simplicity while the legal documents impose real co-owner burdens

- Advisors who present the structure as routine when it requires precision

A TIC is effective when the documents, operations, and tax reporting all align. If they do not, the investor may discover the problem after the exchange is complete, when the options are limited and the tax exposure is already in motion.

The Step-by-Step Flow of a TIC 1031 Transaction

A tenants in common 1031 transaction moves fast, and the time pressure is not forgiving. Investors frequently lose their advantage because they start reviewing the replacement option after the relinquished property has already sold.

Step one starts at the sale

The transaction begins when the investor disposes of the relinquished property. At that point, the seller cannot take possession of the proceeds and decide what to do later.

A Qualified Intermediary holds the exchange funds. That is essential because direct receipt of the proceeds can create constructive receipt, which can destroy the tax-deferred exchange.

The two deadlines that control the deal

The exchange then runs on two federal timing rules referenced in the verified material.

- 45-day identification period. The investor must identify replacement property within 45 days.

- 180-day closing period. The investor must complete the acquisition within 180 days.

Those deadlines matter whether the replacement property is wholly owned or a fractional TIC interest. A sponsor who shows up late with documents, financing issues, or unresolved title questions can create damage.

The legal issue is not just whether the TIC closed. It is whether the investor was funneled into a hurried deal because the advisor failed to plan suitable options before the exchange clock started.

How the TIC interest is selected

In a typical offering, the investor reviews a specific property assembled by a sponsor. The investor is not buying stock. The investor is acquiring an undivided ownership interest in real property.

That review should include:

- The TIC agreement

- The management arrangement

- The financing structure

- Risk disclosures

- Exit and transfer restrictions

- Sponsor compensation and conflicts

Sales practices matter most at this point. A broker may present the property as “passive” while glossing over how limited the exit options are, how much coordination the ownership group may require, or how little control the investor has once the deal closes.

How closing works

At closing, the investor’s exchange funds move through the Qualified Intermediary into the acquisition of the TIC interest. Deeds, exchange assignments, and ownership records must line up with the structure represented to the IRS.

Some investors also hold their TIC interests through a disregarded single-member entity. That can be useful if done correctly, but it does not cure poor drafting, weak disclosure, or an unsuitable recommendation.

The friction points that derail transactions

In practice, the smooth version and the actual version are different.

Common failure points include:

- Late delivery of offering documents

- Unclear lender conditions

- Conflicts between marketing language and legal terms

- Incomplete explanation of co-owner obligations

- Pressure to sign before meaningful review

A competent process gives the investor enough time to evaluate whether the TIC is appropriate at all. A defective process creates urgency first and understanding second. That sequence is how bad recommendations get sold.

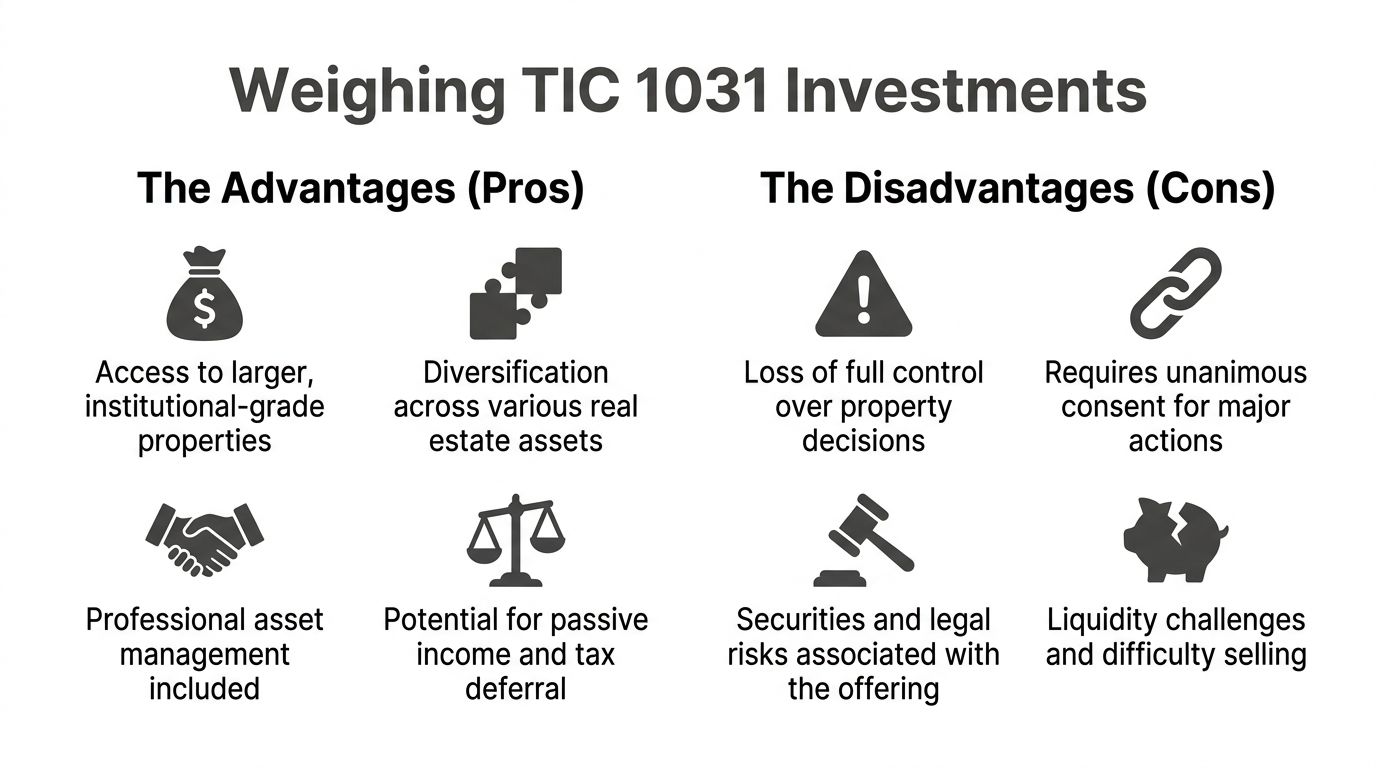

Weighing the Pros and Cons of TIC 1031 Investments

A tenants in common 1031 investment is not good or bad. It is a trade-off. The problem is that the trade-off is presented as one-sided.

What investors usually like

A TIC can solve problems for the right investor.

It can provide access to property types that one investor might not buy alone. It can also allow fractional ownership sizing that is more specific than buying an entire replacement property. Verified material also notes that TIC structures can permit an owner to sell a fractional interest into a new 1031 exchange independently, if the arrangement stays within the governing rules, as discussed in this explanation of how a 1031 exchange works with tenancy in common ownership.

Some investors also value the ability to hold unequal ownership shares rather than matching every co-owner dollar for dollar.

The advertised upside

Here is the favorable version sponsors emphasize:

- Fractional access. Investors can enter a larger asset without buying the whole property.

- Allocation flexibility. Ownership percentages can be adjusted.

- Potential passivity. Day-to-day property operations may be delegated.

- Exchange utility. A TIC can function as replacement property if structured correctly.

Those points are valid. But each one has a matching limitation.

The drawbacks that deserve equal attention

A TIC can be difficult to exit. It can be difficult to value. It can also become contentious when owners have different goals.

The hidden burdens typically include:

| Potential benefit | Matching drawback |

|---|---|

| Fractional ownership | Fractional interests can be illiquid |

| Delegated management | Delegated management can create opacity and sponsor dependence |

| Co-ownership flexibility | Co-ownership can produce disputes over strategy, sale timing, or expenses |

| 1031 compatibility | A rule violation can jeopardize deferral treatment |

One of the biggest problems is psychological. Investors hear “fractional ownership” and think that means convenience. In reality, it frequently means less control, more paperwork, and more dependence on other parties.

The compliance trap hidden inside the upside

The same source that describes the transfer flexibility also warns that management contracts extending beyond one year, or certain buy-sell rights, can create partnership reclassification risk. That is the central tension in many TIC deals. Investors are sold ease and flexibility, but the IRS rules force the structure to remain narrow and disciplined.

If a TIC offering sounds overly simplified, excessively sponsor-controlled, or resembles a packaged business too closely, the investor should ask whether the legal structure still looks like true co-ownership.

Who should be skeptical

Investors should pause when any of the following are true:

- The advisor treats the product as a default replacement property

- The investor needs ready liquidity

- The investor is conservative, retired, or dependent on principal preservation

- The investor was not given time to compare alternatives

- The investor does not fully understand how decisions will be made after closing

A TIC may work for an experienced investor who understands both property aspects and the structural limits. It is a much worse fit when it is sold as a low-friction parking place for exchange proceeds.

Uncovering the Securities and Legal Risks of TIC Deals

The biggest losses in TIC deals frequently do not begin with rent rolls or cap rates. They begin at the point of sale.

Many TIC interests are marketed through brokerage channels or financial advisors as alternative investments. That creates a different set of duties. The recommendation must fit the customer. The risk profile must be explained. Material facts cannot be omitted. Conflicts cannot be hidden. When those duties are violated, the investor may have a claim.

Verified material states that FINRA arbitration data shows a significant rise in disputes involving alternative investments like TICs, often involving unsuitable recommendations, and notes that investors may have legal recourse when brokers fail to disclose risks tied to Rev. Proc. 2002-22, as described in this discussion of tenants in common 1031 exchange litigation concerns.

Unsuitable recommendations

A TIC can be inappropriate even if the documents are technically complete.

That happens when a broker recommends it to someone whose objectives, risk tolerance, liquidity needs, sophistication level, or age make the product a poor match. This issue appears with retirees, seniors, and investors who believed they were moving into something conservative after selling a property.

Examples include:

- A client needing near-term access to funds

- An elderly investor dependent on principal

- A conservative investor placed into a complex illiquid structure

- A client pushed into a TIC without meaningful comparison to other exchange options

A bad suitability analysis does not become acceptable because the investor signed papers.

Misrepresentations and omissions

The second major category is disclosure failure. In TIC cases, that frequently means the advisor highlighted tax deferral and downplayed the rest.

The omitted issues may include:

- Illiquidity

- Restrictions on control

- Sponsor compensation

- Debt risks

- Conflicts of interest

- The possibility that poor structuring could affect tax treatment

- The difficulty of reselling a fractional interest

If the pitch focused on “institutional quality property” and “passive income” while giving little attention to structural hazards, that is a warning sign.

Many investors do not lose money because they knowingly chose a high-risk product. They lose money because the product was framed as safer, simpler, or more suitable than it was.

Sponsor and co-owner problems

Even when the original recommendation was facially plausible, the investment can later unravel through management failure.

Practical examples include:

Operational mismanagement

The sponsor fails to manage the property competently, communicates poorly, or creates unexplained losses.Capital pressure

Investors may be asked to contribute additional funds or face unfavorable consequences.Exit paralysis

The ownership group cannot align on sale timing or restructuring.Bankruptcy or distress involving another party

A troubled participant or related entity can complicate financing, control, or disposition.

TICs are sold as if co-owners exist in the background without issue. In reality, the legal relationships among investors, sponsors, managers, and lenders can become the center of the dispute.

The legal theories that frequently matter

Claims in TIC cases commonly involve:

| Claim type | Core allegation |

|---|---|

| Unsuitable recommendation | The broker recommended a product inconsistent with the client’s profile |

| Misrepresentation | The advisor made affirmative statements that were misleading |

| Omission of material facts | The advisor left out risks a reasonable investor needed to know |

| Breach of fiduciary duty | The advisor put sales interests or conflicts ahead of the client |

| Negligence | The recommendation process fell below professional standards |

Investors trying to understand that process can review a basic explanation of what securities litigation involves and how claims may proceed outside an ordinary property dispute.

Why TIC losses are recoverable claims, not just bad outcomes

Not every failed investment creates liability. But many TIC losses link to avoidable conduct.

That distinction is critical. A vacancy issue or market downturn may be one part of the story. A recommendation made without proper diligence, without fair disclosure, or without suitability analysis is another. In securities cases, the second part drives the claim.

Investors should take a hard look at the sales process if any of the following happened:

- The advisor created urgency based on exchange deadlines

- The investor did not receive a balanced explanation of the downsides

- The product was described as safe, passive, or conservative

- The client was older or risk-averse

- The account already showed overconcentration in alternatives

- The investor learned key facts only after the purchase

Those are not minor complaints. They are the facts that frequently define recoverable misconduct.

Comparing TIC with Delaware Statutory Trusts

For many investors, the main question is not whether a TIC can work. It is whether another 1031 structure would have been more appropriate.

The most common comparison is the Delaware Statutory Trust, or DST. Verified material explains that the market has shifted over time, with DSTs becoming more popular because they offer similar tax benefits with a simpler management structure and fewer operational frictions among co-owners, as discussed in this overview of DST and TIC differences for 1031 investors.

The practical difference

A TIC is direct co-ownership. A DST is a trust structure used to hold investment real property for 1031 purposes.

That difference changes the investor experience.

With a TIC, the legal system tries to preserve direct ownership characteristics. With a DST, the investor is typically seeking a more passive arrangement from the start.

Side-by-side comparison

| Issue | TIC | DST |

|---|---|---|

| Basic structure | Fractional direct ownership in real property | Beneficial interest in trust-owned real property |

| Investor role | Co-owner with rights defined by TIC documents | More passive beneficiary role |

| Management friction | Can be higher because co-owner dynamics matter | Often lower due to centralized structure |

| Use case | Investors comfortable with direct co-ownership complexity | Investors seeking passive 1031 replacement property |

For a deeper look at the product category, investors can review this discussion of 1031 DST investments.

Why this comparison matters in a misconduct case

A broker does not have to recommend the “best” product in the abstract. But the broker does need to recommend a suitable one.

If a client needed simplicity, passivity, and reduced operational friction, the existence of DSTs matters. It raises a fair question. Why was the client placed into a more complicated TIC structure instead?

That question gets sharper when the investor was older, less experienced, or under deadline pressure. It also matters when the advisor did not explain the alternatives in a balanced way.

When the choice itself is the problem

Sometimes the claim is not that TICs are defective. The claim is that the investor should not have been placed into that structure at all.

That is where brokerage liability frequently resides. Not in the abstract legality of the product, but in the mismatch between the product and the person who was sold it.

When to Seek Legal Help for TIC Investment Losses

A common pattern looks like this. The investor sells appreciated property under a tight 1031 deadline, relies on a broker’s recommendation, signs a stack of TIC documents with limited time to review them, and only later learns the investment was illiquid, heavily indebted, or far more speculative than advertised. At that point, the issue is not only whether the property underperformed. The issue is whether the product was sold lawfully in the first place.

A practical checklist

Legal review makes sense when the facts suggest a sales practice problem rather than ordinary investment risk:

- Risk was minimized. The advisor described the TIC as safe, stable, conservative, or close to direct real estate ownership without explaining sponsor risk, debt risk, and co-owner restrictions.

- Liquidity was not explained. You later discovered there was no realistic resale market for your TIC interest and no clear way to value it.

- The exchange deadline controlled the decision. You were pushed to invest quickly because your identification or closing window was about to expire.

- You did not understand the structure. The private placement materials arrived late, key documents were not explained, or you were expected to sign without a meaningful chance to review them.

- The recommendation did not fit your investor profile. You were retired, risk-averse, dependent on principal, or needed access to funds that the TIC structure effectively tied up.

- Important downsides were omitted. Fees, conflicts of interest, financing terms, control limits, concentration risk, or tax-related complications surfaced only after the purchase.

One red flag by itself may not establish a claim. Several of them often justify a closer look.

Why both tax and securities counsel can matter

TIC loss cases often involve two separate tracks. One concerns whether the exchange was structured and documented correctly. The other concerns how the investment was marketed and sold.

If you are sorting through property transaction aspects, a real estate attorney specializing in 1031 exchanges can help evaluate the exchange structure itself. If the core problem is misrepresentation, unsuitable recommendations, omitted risks, or failure to supervise the sale of a complex alternative investment, securities counsel is usually the better fit for evaluating recovery options.

Investors dealing with advisor misconduct can also review what a financial fraud attorney does when losses stem from negligence, unsuitable recommendations, or fraud.

Losses do not end the analysis

Some TIC investments lose value because the property's investment thesis fails. That happens.

But I often see losses tied to conduct that should have been challenged much earlier. Brokers may present TIC offerings as income-producing real estate while downplaying illiquidity, debt exposure, sponsor dependence, and the investor’s lack of practical control. Firms may approve sales to clients who needed a simpler, more liquid investment. In those cases, FINRA arbitration may offer a path to recover damages from the brokerage firm or registered representative.

A poor result does not automatically mean there is a case. A “bad market” explanation does not end the inquiry either. If the recommendation was unsuitable, the disclosures were incomplete, or the firm failed to supervise the sale properly, the investor may have a viable claim.