A lot of investors arrive at this issue the same way. A broker or advisor presents options as a smarter way to generate income, hedge a portfolio, or make a stagnant account “work harder.” The language sounds controlled and professional. Then the losses come fast, the account statements become harder to follow, and the explanation shifts from confidence to blame.

If that sounds familiar, your losses may not be just a market story. They may also be a supervision, suitability, or disclosure story. That distinction matters, because ordinary investment risk is one thing. Recommending complex, time-sensitive, strategies with amplified risk/reward to the wrong client, or without full disclosure, is something else entirely.

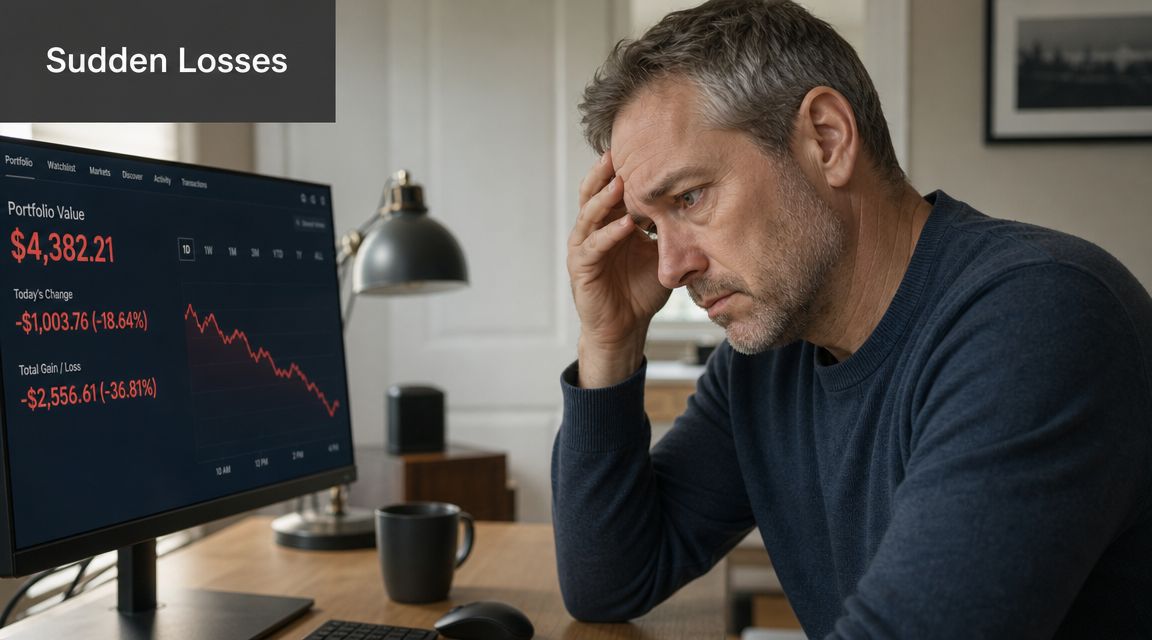

The Growing Danger of Options for Everyday Investors

A common scenario looks like this. An investor nearing retirement tells an advisor they want income and limited risk. The advisor suggests selling options, buying short-dated calls, or using spreads described as “conservative” or “enhanced yield.” At first, the trades seem manageable because each position may look small in isolation. But options don't behave like ordinary stock holdings. A few bad expirations, an assignment, or a volatility shock can turn a controlled-looking strategy into a serious account drawdown.

That problem has grown as more nonprofessional investors entered the options market. The NYSE's review of options trading trends states that retail accounts represented about 34% to 38% of options trading in late 2019, reached 48% in July 2022, and remained about 45% in July 2023. The same NYSE analysis estimated retail accounts made up about 34% of options trading in contracts with roughly 1 to 3 months to expiration, which matters because these trades are highly sensitive to time and volatility.

Why this matters in practice

When retail participation rises in short-term options, more investors face risks that many didn't fully bargain for. The problem isn't just complexity on paper. It's speed. A stock investor can be wrong and still have time. An options investor can be right about direction and still lose because the move came too late.

Investors often see a similar pattern in other products offering magnified exposure marketed as tactical tools, including leveraged and inverse ETFs. The product sounds complex. The actual risk sits in daily movement, the amplification of outcomes, and how the advisor uses it in a real account.

Many investors don't realize the legal question isn't whether options are risky. They are. The legal question is whether the broker had a reasonable basis to recommend that risk to you.

The issue is often advice, not just volatility

Losses alone don't prove misconduct. But certain facts should make you pause. Were you looking for income, preservation, or moderate growth? Did your advisor gloss over margin, assignment, or expiration mechanics? Were trades frequent enough that the account felt like it needed constant rescue?

Those details often separate ordinary market loss from a recoverable claim.

Understanding the Fundamental Options Trading Risks

Options are contracts with terms, deadlines, and payoff rules. That makes them different from buying shares of stock and waiting. If you own stock, the position doesn't expire. If you buy an option, time is part of the risk from the day you enter the trade.

FINRA states that options risks vary by strategy, but can include “significant risk of loss beyond your initial investment,” and it specifically identifies margin risk, assignment risk, and expiration risk for certain positions in its investor guidance on options. That's the language regulators use, and it's important because it confirms these products are structurally different from simple stock ownership.

Time can beat you even if the market doesn't

One of the hardest concepts for investors is time decay, often discussed as Theta. An option contains extrinsic value that erodes as expiration approaches. That erosion accelerates in short-dated contracts, as explained in Public's discussion of time-decay risk in options.

Here's the practical consequence. You can buy a call because you think a stock will rise. The stock may even drift upward. But if it doesn't move far enough, fast enough, the option can still lose value as the clock runs out.

The premium isn't a deposit

Many investors hear “your risk is limited to the premium” and treat that as reassuring. Legally and financially, that statement is incomplete. The premium is not a placeholder you get back if the trade doesn't work. For a long option buyer, that amount is typically the full amount at risk.

That matters because people often compare an option purchase to buying stock. They are not comparable in the way many sales pitches suggest.

- Stock ownership: You own the asset and can usually continue holding it unless you choose to sell.

- Long option purchase: You own a contract with an expiration date. If the expected move doesn't happen in time, the contract's value can shrink or disappear.

- Complex options position: You may also face assignment, exercise, and timing issues that don't exist with ordinary stock purchases.

Practical rule: If the strategy needed a chart, multiple Greeks, or daily management to make sense, it probably wasn't a plain-vanilla investment recommendation.

A useful example of how these issues show up in disputes appears in this discussion of options-related investment loss recovery. The lesson isn't that every options loss is wrongful. It's that many investors were never given a fair explanation of how quickly these contracts can fail.

How Leverage and Margin Can Amplify Your Losses

A loss in an options account can turn into an account crisis very quickly when a small cash outlay controls a much larger market exposure. Investors are often shown the lower entry cost. They are not always shown how fast percentage losses can build, or how little room there is for error once the position moves the wrong way.

For a buyer of calls or puts, the entire premium can be lost. For an investor who sells an uncovered call, the risk is far worse. FINRA's investor education materials on call options and liquidating stock help illustrate the core problem. Some options positions have a defined maximum loss. An uncovered call does not have a natural ceiling if the stock keeps rising.

That difference matters in investor claims. I often see account records where the recommendation was framed around income, high probability, or a way to "reduce cost." The legal question is more concrete. Did the broker clearly explain the exposure, and did that exposure fit the client's finances, experience, and tolerance for loss?

Why uncovered positions are so dangerous

An uncovered call creates an obligation to deliver shares the investor does not own. If the stock jumps, the investor may have to buy shares at a much higher price to satisfy assignment. Profit is capped at the premium received. The loss can continue growing as the stock rises.

That is not a technical footnote. It is often the heart of the dispute. A retiree looking for income and capital preservation should not be placed into a strategy that can expand losses far beyond what the investor expected or could afford.

Margin can force the worst possible outcome

Margin changes the power dynamic in the account. Once borrowed funds or maintenance requirements apply, the firm can demand more collateral, close positions without waiting for the investor's consent, and do so during stressed market conditions. The trade may still have time left. The investor may still believe the position can recover. The firm may liquidate anyway.

If you need the mechanics in plain English, this explanation of what triggers margin calls and how firms liquidate positions is a useful place to start. In practice, margin often converts a paper loss into a realized loss at the worst moment, especially in volatile options accounts with concentrated positions.

Some investors also find it helpful to see that this issue is not unique to one regulator or one market. This discussion of FCA margin rules UK highlights the same basic reality. Firms focus on collateral coverage and liquidation rights. Investors focus on whether the trade can still work. Those interests separate quickly during a market drop.

From a legal standpoint, that separation matters. If a broker recommended margined options trading without a fair explanation of forced liquidation risk, account concentration, or the investor's need for ready cash, the loss may involve more than market risk alone.

When Investment Risk Becomes Broker Negligence

Your advisor told you the options strategy was controlled, income-focused, or temporary. Then the losses kept coming, positions turned over faster than you could follow, and the account no longer resembled the plan you thought you approved. That fact pattern matters. Many options losses are market losses. Some are the product of recommendations that never fit the investor in the first place.

FINRA's suitability rule requires brokers to have a reasonable basis for a recommendation and to match that recommendation to the customer's profile, including age, financial circumstances, investment objective, risk tolerance, liquidity needs, and experience. FINRA explains those duties in its Suitability Rule 2111 guidance. In options cases, the legal question is often straightforward. Was this investor placed into a strategy the broker could fairly recommend to this customer, in this account, with these risks?

That is where many firms have trouble. The defense usually starts with signed forms and generic disclosures. The claim usually turns on what happened.

What suitability means in plain English

A suitable recommendation fits the person, not just the product category. A retiree seeking income and preservation should not be treated like an active trader with spare capital, trading experience, and the ability to absorb sharp losses. If the account objective was conservative or moderate, repeated options speculation can conflict with the client's stated needs even when each individual trade is described as a hedge, enhancement, or short-term opportunity.

Paperwork does not fix that problem by itself. I often see account forms that overstate options experience, risk tolerance, or net worth after a strategy has already been sold. Those forms are relevant, but they are not the whole case. Emails, call notes, trade patterns, and monthly statements often give a more honest picture of what the investor was told and whether the broker was steering the account into activity the client did not understand.

Red flags investors should take seriously

Misconduct usually appears as a pattern. One bad trade may be bad luck. A series of recommendations that ignore the investor's profile is something else.

| Red Flag | What It Looks Like | Why It's a Problem |

|---|---|---|

| Conservative investor placed in speculative options | The client asked for income, preservation, or moderate growth, but the advisor recommended active options trading or uncovered positions | The recommendation may not match the client's profile or financial capacity for loss |

| Risks minimized | The broker used reassuring labels but did not fairly explain assignment, expiration, early loss, or how quickly positions could deteriorate | A client cannot make an informed decision without a fair explanation of material risks |

| Constant rolling or short-term trading | Expiring positions were repeatedly replaced, often after losses, with little pause or reassessment | The account can be drained by repeated commissions, poor timing, and mounting exposure |

| Account activity too complex to monitor | The investor could not track entries, exits, and replacement trades without outside help or a streamlined trading workflow | Complexity can hide unsuitable trading and make meaningful consent doubtful |

| Documents that do not match reality | New account forms show aggressive objectives or extensive options experience the client never discussed | Inaccurate profile information can be used later to defend recommendations that never fit |

| No meaningful supervision | The losses mounted, turnover continued, and no one at the firm interrupted the pattern | Firms have their own supervisory duties, separate from the broker's conduct |

| Trades the client did not clearly authorize | Positions appeared that the investor did not understand, approve, or learn about until after execution | Unauthorized trading can support a separate claim for recovery |

If your account started to look like a speculative trading program instead of a personal investment plan, the issue may be broker conduct, not market timing.

What tends to help a legal claim

Specific facts matter more than outrage. Identify who recommended the trades, what your investment objective was, what you were told about risk, and how the strategy changed over time. A strong claim usually ties losses to concrete conduct such as unsuitable recommendations, misstatements, unauthorized trading, excessive activity, or weak supervision.

General complaints that the market was unfair rarely go far. Records do. That is why investors should focus on account statements, confirmations, account opening forms, text messages, emails, and notes of calls with the advisor.

Kons Law represents investors in disputes involving broker misconduct, unsuitable recommendations, and FINRA arbitration claims. The legal value comes from matching the trading record and communications to recognized duties under industry rules and securities law.

Your First Steps for Documenting Trading Losses

Investors often hurt their own cases by waiting too long or collecting the wrong material. Start with records, not conclusions. You don't need to prove the entire claim before speaking with counsel, but you do need to preserve the documents that show what happened.

Build a clean file before memories fade

Create one folder for account statements, one for trade confirmations, and one for communications. Include emails, text messages, notes from phone calls, screenshots from the brokerage app, and any brochures or slide decks the advisor used when recommending the strategy.

If you tracked activity in a spreadsheet or app, preserve that too. Even tools built for a more streamlined trading workflow can help reconstruct the sequence of entries, exits, and rolling trades. The point isn't to prove sophistication. It's to preserve chronology.

Focus on the documents that reveal suitability

Some records carry more legal weight than investors realize:

- New account forms: These often state your objectives, risk tolerance, liquidity needs, and options experience.

- Options agreements and approvals: They may show what level of options trading the firm approved and when.

- Monthly statements: These reveal concentration, turnover, margin use, and the pace of losses.

- Trade confirmations: They identify the exact contracts, dates, and position types involved.

- Written communications: These often contain the clearest evidence of what the broker promised or failed to disclose.

Save the earliest communications you can find. The first recommendation often reveals more than later explanations written after losses began.

Write a timeline in ordinary language

A good timeline doesn't need legal jargon. Start with when you opened the account, what you told the advisor you wanted, when options trading began, and when the losses accelerated. Note any conversations about “income,” “safe hedging,” “temporary drawdowns,” or requests to add money because of margin pressure.

Keep the timeline factual. Avoid guessing about motives. A sentence like “On or about this month, my advisor recommended selling calls for income and told me the risk was manageable” is better than a long argument about fraud.

That file becomes the foundation for an attorney's review.

Pursuing Recovery Through FINRA Arbitration

Most disputes between investors and brokerage firms don't proceed in court. They go through FINRA arbitration, which is the forum commonly required by brokerage account agreements. For many investors, that sounds intimidating at first. In practice, it's a familiar path for securities counsel and a structured process for resolving these claims.

A useful overview of the FINRA arbitration process explains the basic mechanics in plain language. The key point is that arbitration is not an informal complaint desk. It is the main venue where investors pursue recovery against broker-dealers and registered representatives.

What the process usually involves

The case begins with a written filing that explains who the parties are, what happened in the account, and why the losses are believed to be recoverable. That document is often called a Statement of Claim.

After that, the parties exchange documents. This stage matters in options cases because it often reveals account-opening records, notes, supervisory reviews, internal communications, and compliance materials that the investor never saw.

A hearing may follow if the matter doesn't resolve earlier. Witnesses testify, documents are presented, and the arbitrator or panel decides liability and damages.

Why investors shouldn't assume they have no case

Many people delay because they think signing forms or receiving disclosures means they've waived everything. That's often too simplistic. Firms still have duties. Advisors still have obligations when they recommend strategies, characterize risk, use margin, and manage the account over time.

Here are the practical questions an attorney usually asks early:

- What were your stated objectives when the account was opened?

- What options strategy was recommended, and how was it described to you?

- Did the account use margin or involve rapid, repeated trading?

- Do the account forms accurately reflect your experience and risk tolerance?

- What written communications exist before and after the losses?

Arbitration is often less about proving that options are dangerous and more about proving that this broker used them improperly in this account.

The clearer your records, the stronger that presentation becomes.

Take Control and Explore Your Recovery Options

Options trading risks are real even when everyone behaves properly. But that truth sometimes gets misused. Brokers and firms may point to the existence of risk as though it excuses every recommendation, every omission, and every account-level failure. It doesn't.

If your advisor pushed options as income, understated the risk amplification, used margin without clear warning, or kept rolling short-term trades while losses mounted, you shouldn't assume that what happened was just bad luck. The most important question is whether the strategy matched your needs, your experience, and your ability to bear the loss.

That is where recovery begins. First, understand the product. Second, examine the recommendation. Third, preserve the record before more evidence disappears.

If you're worried about the cost of asking a lawyer to review what happened, even a general resource like this guide to legal consultation costs for SMEs can help frame the question. In investor-loss matters, the key isn't whether you can recite options terminology. It's whether a securities attorney can connect your documents to a viable claim.

You don't need to solve the case by yourself. You do need to act while the records are available and the events are still reconstructable.

If you'd like to discuss whether your options trading losses may be recoverable, contact Kons Law for a free, no obligation consultation at (860) 920-5181. A securities attorney can review your account documents, assess whether broker misconduct may have contributed to the losses, and explain the investment loss recovery process.