A bad investment rarely starts with a dramatic warning. It usually starts with trust. Your advisor sounded confident. The product was framed as appropriate for retirement, income, or safety. Then the account value dropped, the fees felt impossible to untangle, and you started wondering a simple question that should have been clear from the beginning.

Was this person even licensed to sell me this?

That question matters more than most investors realize. In securities cases, licenses are not paperwork trivia. They define the products a broker may recommend, the states where that broker may solicit clients, and the rules that govern suitability. When those limits are ignored, the misconduct often shows up later as losses, overconcentration, unauthorized sales, or advice that never matched the investor’s needs in the first place.

Navigating Your Investments and Your Advisor's Credentials

Most investors do not review an advisor’s credentials before opening an account. They rely on the firm name, the office setting, and the reassurance that “this is standard.” That is understandable. It is also why unsuitable sales can sit unnoticed for years.

The practical issue with series 6 and series 63 is that they answer two different questions. One asks what a broker can sell. The other asks whether the broker is properly registered to do business under state law. If you are holding mutual funds, variable annuities, or similar packaged products and the recommendations now seem questionable, those license boundaries are a good place to start.

Why investors should care

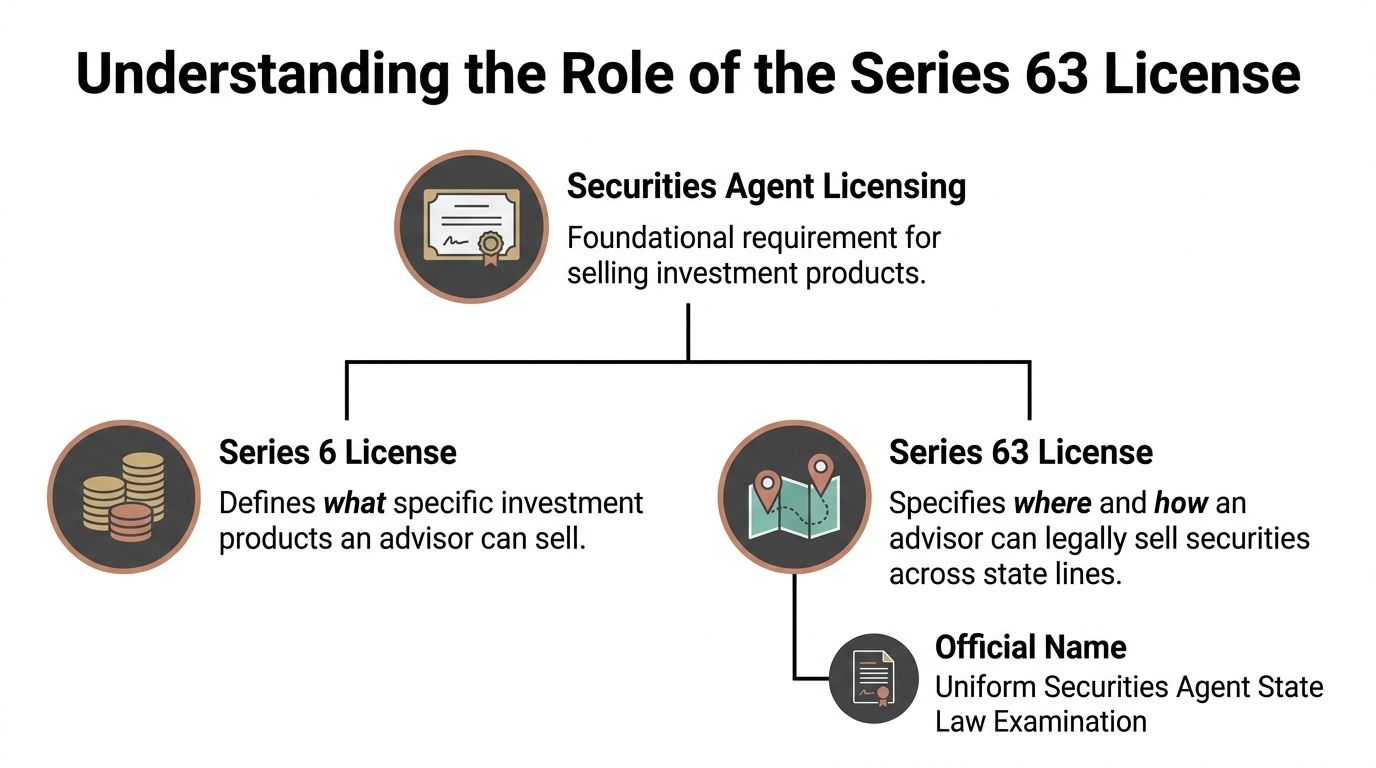

A Series 6 license is limited. A Series 63 license is about state law authorization and conduct. Together, they can tell you whether the sale was within the broker’s legal lane or outside it.

That distinction becomes important when an investor later discovers one of these problems:

- The product never fit the account’s purpose. A retiree seeking liquidity ends up in a variable annuity with surrender charges.

- The recommendation exceeded the broker’s authority. A broker with only a narrow product license moves into alternatives or other products outside that scope.

- The solicitation itself may have been improper. The broker worked across state lines without proper registration.

If you are unsure whether your broker acted as a salesperson or as a fiduciary-style adviser, this explanation of the difference between a broker and investment advisor can help frame the issue.

Key takeaway: Investors often focus first on losses. In practice, the better first question is whether the recommendation was authorized, suitable, and legally made.

What this means for a potential claim

In arbitration and litigation, license limits can support claims for unsuitability, negligent supervision, unauthorized recommendations, and sales outside the broker’s permitted scope. They can also expose failures by the brokerage firm that employed or supervised the broker.

For an investor, that is empowering. You do not need to master every securities rule. You need to understand enough to identify red flags and preserve the documents that show what happened.

What the Series 6 License Really Authorizes

The clearest way to understand a Series 6 license is to treat it like a specialty permit. It does not authorize a broker to sell every security. It authorizes a limited menu of packaged investment products.

That usually includes mutual funds, variable annuities, and variable life insurance premium funding programs. It does not extend to individual stocks or bonds, which require the broader Series 7 authority.

What the exam tells you about the license

The exam itself reflects that narrower focus. The Series 6 exam consists of 50 scored questions, must be completed in 90 minutes, and requires a 70% passing score, with a first-time pass rate of about 58%, compared with 82% for the Series 63, according to Open Exam Prep’s comparison of Series 6 and Series 63.

That matters because the tested material is not random. It centers on packaged products and suitability issues such as mutual fund share classes, surrender charges, and matching the product to the investor’s profile. In other words, the license is built around selling a specific category of product, not around universal securities authority.

What a Series 6 holder cannot do

For investors, the forbidden side of the license is often more important than the permitted side.

A broker holding only Series 6 should not be recommending or selling:

- Individual stocks

- Corporate bonds

- Options

- Private placements

- Non-traded REITs

- Other non-packaged alternatives outside the license scope

If your account statement shows those products and the broker had only Series 6 authority, that is not a technicality. It can be evidence that the recommendation fell outside the broker’s licensed authority.

Practical tip: When a broker says, “I can help with all investments,” compare that claim against the products in your account. The statement often tells a different story.

Why this matters in annuity cases

Series 6 problems do not only arise when a broker sells something clearly forbidden. They also arise when a broker sells a permitted product badly.

A variable annuity may be within the license scope, but that does not make it suitable. Investors often run into problems involving high fees, long surrender periods, duplicate benefits inside retirement accounts, or exchanges that benefit the salesperson more than the client. FINRA has specific conduct rules in this area, especially for deferred variable annuities, which is why investors dealing with these products should understand FINRA Rule 2330 and annuity sales obligations.

The practical lesson is simple. A broker can be licensed to sell a product and still recommend it improperly.

Understanding the Role of the Series 63 License

The Series 63 is different. It is not mainly about product expertise. It is about state law permission and the rules governing how securities business is conducted.

If Series 6 answers what a broker may sell, Series 63 addresses where the broker may legally solicit and transact business, along with the ethical framework that applies under state securities law.

Why state registration matters

State securities laws, often called Blue Sky laws, are designed to protect investors from fraud, misrepresentation, and unlawful sales activity. A broker can have product authority and still have a state registration problem.

That becomes important when the relationship crosses state lines. Maybe your advisor was based in one state, your retirement account was in another, or the broker changed firms and continued to solicit you after a move. Those details matter.

A useful starting point for investors is understanding what Blue Sky law means in securities disputes.

A growing interstate compliance issue

This is not a theoretical problem. According to Financial Planner World’s discussion of FINRA exam issues, recent FINRA data shows a 15% rise in disputes over unregistered interstate sales of BDCs and non-traded REITs, often involving brokers with partial Series 63 waivers.

For investors, that trend points to a familiar pattern. The broker acts first, the compliance questions come later, and the investor gets left holding a product that should never have been sold in that manner.

What Series 63 can reveal in a claim

A Series 63 issue can support several arguments in a dispute:

- Improper solicitation in your state

- Failure to comply with state anti-fraud requirements

- A supervision failure by the brokerage firm

- Unauthorized interstate sales activity

The investor does not need to prove every registration detail alone. But if a broker was not properly registered where the sale occurred, that fact can strengthen a claim and increase pressure on the firm to explain why the sale went forward.

Key Differences Series 6 vs The Broader Series 7

Investors often hear that an advisor is “licensed” and assume that means licensed for everything. It does not. The practical comparison is between the narrow Series 6 and the much broader Series 7.

A Series 6 holder is limited to packaged products. A Series 7 holder has authority for a far wider range of securities activity, including individual securities and more complex products. For an investor reviewing losses, this comparison helps answer a basic question. Was the broker acting inside the boundaries of the license they held?

License comparison in practice

Below is the simplest way to think about it.

License Comparison: What Your Advisor Can Sell

| Product / Activity | Series 6 Holder | Series 7 Holder |

|---|---|---|

| Mutual funds | Yes | Yes |

| Variable annuities | Yes | Yes |

| Variable life insurance premium funding programs | Yes | Yes |

| Individual stocks | No | Yes |

| Individual bonds | No | Yes |

| Options | No | Yes |

| Private placements | No | Yes |

| Direct participation programs such as oil and gas partnerships | No | Yes |

| Broad general securities activity | No | Yes |

Where investors get hurt

In real disputes, this difference matters most when the portfolio contains products that do not belong with a Series 6-only broker.

Examples include:

- A retiree is sold a private real estate deal by a broker whose registration only supports packaged products.

- An account is loaded with individual technology stocks even though the broker lacked broad securities authority.

- The broker recommends a BDC or non-traded REIT while presenting it as just another income product.

Those are not minor compliance errors. They go to the heart of whether the recommendation was authorized at all.

Scope problems often overlap with suitability problems

The most persuasive investor claims usually do not rely on one issue alone. They combine multiple problems.

A recommendation outside the broker’s license scope often appears alongside one or more of these facts:

- The product was illiquid.

- The investor needed conservative income.

- The account was overconcentrated.

- The risks were poorly explained.

- The firm failed to supervise the broker’s activity.

Key takeaway: When a broker sells beyond the limits of a Series 6 license, the issue is not just authority. It often shows the sales process itself was careless, aggressive, or both.

Why firms still let this happen

Brokerage firms do not escape responsibility by blaming one representative. Firms are expected to supervise product sales, registrations, and suitability. If an investor was placed into products outside a broker’s authority, a common follow-up question is why the firm approved the transaction, paid the commission, and left the account in place.

That is especially important in claims involving alternative investments. Those products often carry limited liquidity, valuation issues, and risk disclosures that ordinary investors do not fully see at the point of sale. If the broker lacked the proper breadth of licensing, that fact can become a direct window into weak supervision.

For investors reviewing statements years later, the practical move is to line up each product in the account against the broker’s actual licenses. That exercise often reveals whether the story told at the sale matched the authority the broker had.

Investor Red Flags and Unsuitable Sales

When investors suspect misconduct, they often focus on performance first. That is understandable, but poor performance alone does not prove a claim. The better approach is to identify whether the broker broke the rules that were supposed to protect you.

License limits are one of the clearest starting points.

Red flags tied to series 6 and series 63

Some warning signs appear on the face of the account history.

Out-of-scope recommendations

If a broker with only Series 6 authority recommended a product outside packaged securities, that is a serious problem. It can show the broker stepped beyond the scope of the license.State registration mismatches

If the broker solicited you from another state, changed firms, or serviced the account after relocation, registration issues may be in play.One-product retirement planning

Investors nearing retirement sometimes find that too much of the account was placed into one product family, especially variable annuities or the same group of mutual funds.

Suitability is not optional

The Series 6 content outline requires advisors to evaluate a client’s financial profile before making recommendations, and that function carries 20% of the exam content, directly tying the license to suitability obligations under FINRA Rule 2111, as discussed in Ironclad Law’s review of Series 6 and Series 63.

That is important in practice. If a broker with only Series 6 recommended a non-packaged product like a BDC, that can be powerful evidence of both an unsuitability claim and a breach of license scope.

What unsuitable sales look like in real accounts

Unsuitable sales are rarely labeled as such. They tend to show up through patterns:

Liquidity was ignored

You needed access to funds for health care, living expenses, or a home sale, but the recommendation locked money up or imposed surrender charges.Risk tolerance was overstated

The account forms may say “moderate” or “growth,” but your real objective was preservation or income.The broker sold what they had, not what fit

This happens often with narrow-license representatives who stay inside a limited shelf of products and force every client into the same menu.The account became concentrated in a single strategy

A retirement account built around one annuity, one sponsor family, or one type of income product may reflect sales pressure rather than sound portfolio construction.

Practical tip: Ask for the new account form, any risk-tolerance questionnaire, and every document signed at the time of purchase. Those records often conflict with what the investor was told.

Why these facts matter in FINRA arbitration

Arbitrators do not need abstract theories. They need a clear story supported by documents. License limits help create that story.

If the broker lacked proper authority, failed to evaluate your financial profile, recommended an unsuitable product, or solicited in a state without proper registration, those facts can support claims against both the individual broker and the supervising firm.

That is why investors should not dismiss license details as back-office formalities. In the right case, they are among the strongest pieces of evidence available.

How to Verify Your Broker's Licenses and History

You do not have to rely on the broker’s business card or title. FINRA’s BrokerCheck lets investors review a broker’s exams, registrations, employment history, and disclosures.

A simple review process

Use this process when you suspect a bad sale or just want to audit the relationship.

Search the broker’s name on BrokerCheck

Confirm you have the correct person and firm.Review the examinations section

Look for whether the broker passed Series 6, Series 7, Series 63, or other relevant exams.Check current and past registrations

Focus on whether the broker was registered where you lived when the recommendations were made.Read the disclosures carefully

Customer complaints, regulatory events, terminations, and judgments can reveal patterns.

Why the CRD number matters

Each registered broker has a CRD number, which helps distinguish brokers with similar names and ties records together across firms and time periods. If you are unfamiliar with that system, this explanation of what a CRD is and why it matters is useful.

What to save

When you find something concerning, preserve it.

- BrokerCheck report

- Account statements

- Trade confirmations

- Emails and text messages

- New account forms and suitability documents

Do not assume the firm will keep everything easy to access. Save copies while they are available.

Key takeaway: BrokerCheck will not prove the entire case by itself, but it can quickly reveal whether the sales story matches the broker’s actual license profile.

Your Path to Recovery After Investment Losses

If you suspect a broker sold you an investment outside their authority, ignored your risk profile, or solicited you without proper registration, the next step is not to argue with the firm’s branch office. The next step is to assess the case the way a securities attorney would.

That means matching the product sold, the account objective, the broker’s licenses, the state registrations, and the paper trail. When those facts do not line up, the investor may have a strong basis to pursue recovery.

When arbitration becomes the right forum

Many brokerage disputes are resolved through FINRA arbitration rather than court. That process can allow investors to pursue claims involving unsuitable recommendations, unauthorized trading, negligent supervision, misrepresentation, and sales outside license scope.

A strong claim usually starts with a focused document review:

- the broker’s registrations

- the dates of the recommendations

- the account opening paperwork

- the concentration and risk profile of the portfolio

- the losses tied to the challenged products

Do not wait for the firm to define the issue

Firms often frame a case as market loss, investor misunderstanding, or normal volatility. That framing can obscure the underlying problem. If the broker lacked the right authority or sold a product that never fit your objectives, the issue is not that the investment went down. The issue is that it should not have been sold to you that way in the first place.

Investors who act early preserve more evidence, clarify the registration history, and put themselves in a better position to evaluate damages and legal options.

If you would like to discuss whether a broker’s licenses, product recommendations, or state registrations may support a recovery claim, contact Kons Law at (860) 920-5181 for a FREE, NO OBLIGATION consultation about the investment loss recovery process.